Disclaimer: Please note this article is not financial advice. The purpose of our blog is purely educational, so please consult a professional accountant or financial advisor before making any financial decision.

So you’ve started a small online business. You are now among the millions who have braved the ecommerce world. Since ecommerce is so complex, and the sheer volume of transactions can be intimidating, your accounting may need help to keep up with your online store. This is where choosing the best accounting software can be worth it.

Accounting software programs can do more than track the inflow and outflow of cash. You’ll be amazed at how they can be a one-stop shop for many of your digital needs, making them worthy of every penny you invest.

So, what’s the best small business accounting software for you? Find out all the answers here in this guide. But first, let’s talk about everything you need to know about ecommerce accounting.

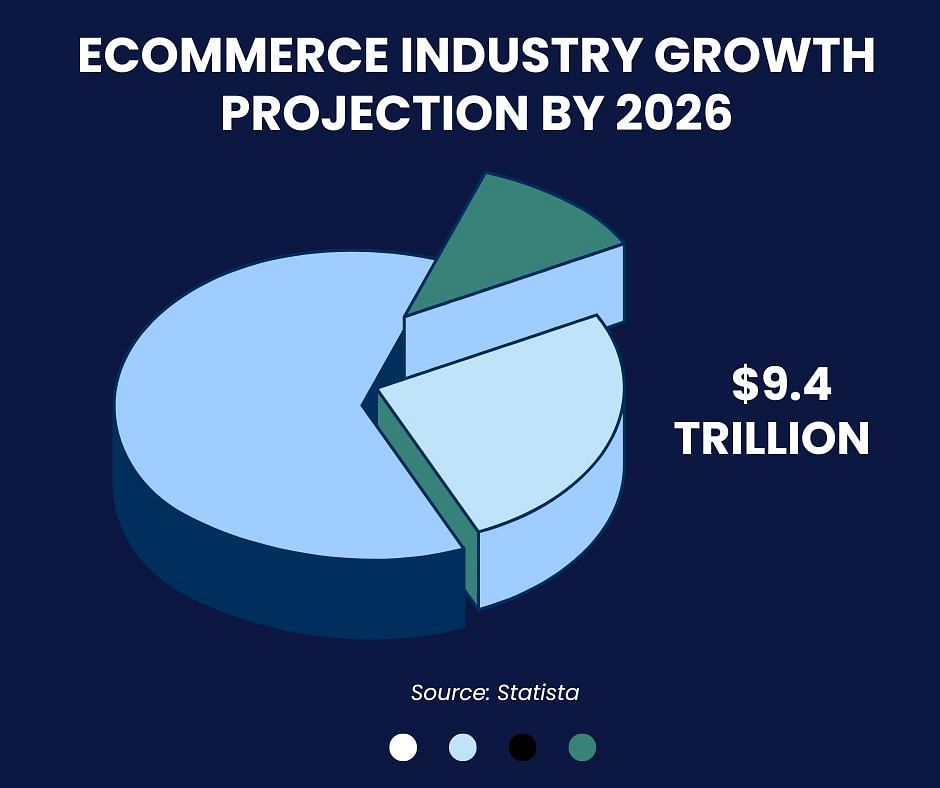

Ecommerce is a worldwide business. In fact, Statista already presented compelling data, showing its global reach and exponential growth. Just think of the transactions that make up this figure—massive.

Given the wide reach, ecommerce accounting differs because there is so much more to account for. Take a look at some of them.

An online business can sell anywhere in the world through an ecommerce platform and exemplary shipping service. But to be able to sell legally, there must always be a sales tax attached to each sale.

Ecommerce accounting requires sales tax calculation for different tax policies. For example:

| Amazon can handle your taxes through Amazon Tax Exemption Program (ATEP) for sales in the US. But you'll still have to collect and remit your sales taxes in Canada. |

On top of that, the US and Canadian sales tax rates are completely different, with tax returns filed each year. Tax management is daunting, requiring careful attention and consideration.

Another thing that separates ecommerce from regular businesses is the vast inventory. Inventory tracking is no easy task for anybody, especially for small-scale startups. You need to have many products on-hand and ready to meet demand at a moment’s notice.

There will also be an inevitable addition to your accounting load, especially if you’re a business that ships to customers in different timezones. Add to that the sheer volume of items you’ll have to check on—where they are stored, how many are ready for shipping, how many are damaged or lost—and regularly reconcile in your records.

If you sell products or services worldwide, expect to see thousands of business transactions daily. That means various modes of payments, currencies, bank accounts, taxes, and so on.

Tracking each transaction will take copious amounts of time and energy. You might miss out on some financial data, which, for a global business, you cannot allow to happen.

While it's possible to do your accounting manually, tracing every ecommerce transaction can make even the best accountants dizzy. Giving your accounting specialist some much-needed assistance, like online accounting software, is recommended.

In addition to maximizing your time and resources, here are eight reasons accounting software is worth it for your small ecommerce business.

A bookkeeper can rely on accounting software to record transactions. Through it, they can take note of all business transactions involving money. They can ensure that income and expenses from different channels, like bank and credit cards or online payment gateways, are all accounted for.

Because of the high-tech tools available today, a bookkeeper’s task of typing data is slowly disappearing. Data from different sources can be connected to a central accounting system. There are also optical character recognition tools that minimize manual data entry.

Invoicing is an essential part of bookkeeping and accounts receivable management. Through software, you can conveniently send payment reminders to customers—all online. Simply schedule the sending date and time and let the software handle its transmission. If customers forget to pay, sending a nudge can also be done on the software.

Invoicing from an accounting tool also makes payment easier for customers as each invoice includes a “Pay Now” button. Customers can click on it for online payment. All money coming from this channel will automatically be recorded in the books.

The money you collect from customers and use to pay suppliers and expenses are all recorded in your business bank account. Through accounting software’s bank connection feature, you can have visibility on these transactions, and they will also be categorized into income and expenses in the books.

Bank reconciliation becomes a seamless process, as you can easily compare the details recorded in your books with the transactions listed in your bank statement. With this, you’ll be able to correct any mistakes and raise red flags on fraudulent deals.

Business planning and forecasting are vital as they allow you to see how your business will go in a projected period. It may not be 100% accurate, but you can still get the closest possible financial situation your business will see in the future.

Many accounting software has a feature that allows you to develop a business financial forecast in just a few clicks. Acquiring past and present numbers won’t be a problem as they are all recorded in the books.

Once you have the forecasted data, you can create plans based on numbers and even simulate results using the software. You can follow a strategy that gives you the best results from there.

The younger your business is, the more often you should generate financial reports. You must regularly check its financial health to adjust your strategies. Good financial reporting contains the following:

| Financial Reports | |

| Balance Sheet | Quickly check your assets, liabilities, and equity using this report. |

| Income Statement | Also known as the Profit and Loss Statement or Statement of Revenue and Expenses. This report shows your business's profit and how income and expenses impact it. |

| Cash Flow Statement | This report illustrates how money flows in and out of your business, showing your earnings and expenditures. |

| Statement of Owner’s Equity | For sole proprietors, this report displays earnings or profit and retained earnings. For corporations, it is referred to as Shareholder’s Equity. |

When you know these reports, you and your accountant can run and analyze them.

As mentioned earlier, inventory is a part of your company assets. You don’t want your customers disappointed because products are out of stock. This is where accounting software comes into play.

Accounting software isn’t only for numbers; it’s for your items too. When you can monitor your inventory, you’ll know which items fly off the shelves and which don’t move. You can also use the information to create plans to duplicate your successes and sell slow products.

Taxes are inevitable, but you can make them manageable. On top of calculation and collection, the best accounting software can handle tax remittance. You can integrate the data from these tools into your accounting system for tracking purposes.

Calculating your tax base and rate becomes easier regarding income tax returns, given the recorded income and expenses in the books. With the most comprehensive accounting software, tax season will be a breeze.

Ecommerce functions online. Data security and protection are indeed vital features you’ll look for in small business accounting programs. Luckily, online financial accounts are protected with cloud-based features.

Traditional accounting using Excel sheets stores books on computers. Still, cloud-based software has more advanced security features and can store information in the cloud. The cloud encrypts data, ensuring hackers and unauthorized individuals cannot access your accounting data. Corruption of data is also less likely.

Most cloud-based software have multiple users and role-based access, meaning only individuals you authorize can access the books.

Besides bookkeeping, inventory, cloud, and tax management, consider examining these features when selecting the most suitable accounting software solution for your business.

Any small business owner should have an accounts receivable feature in their software, given that payments are often made remotely with various payment schemes.

An accounts receivable lets you know how much money to expect and how much you can use to repurchase stock. It also tells you how much your business is shelling out weekly or monthly.

For example: If you're in the retail business, you may have scheduled shipments to replenish your inventory. Accounts payable notes this in advance for you to continue or change, depending on your decision.

Direct integration is also a crucial feature to look for in accounting software. It allows smooth alignment with the ecommerce platforms you've chosen for selling your products. The software can efficiently capture and organize all relevant accounting data by directly integrating with your online stores.

It also ensures that your accounting records are automatically updated in real time, reducing the risk of errors. With direct integration, you'll have an easier time keeping a thorough and accurate overview of your financial performance.

A mobile app functionality is a great feature to add to your accounting software. With everyone on the go nowadays, having a mobile app handy allows you and your staff to update your accounting whenever and wherever.

Being a startup, you can always pick the small business accounting software that can currently satisfy your financial management needs. But you must also choose the one that can scale to more advanced features as you grow your venture.

Here are popular accounting software ideal for ecommerce startups.

The most popular small business accounting software. It has all the features you need. When you sign up for a plan, it’ll backtrack all your financial transactions and do live bookkeeping moving forward.

QuickBooks has:

Xero is another accounting software that will surely ring a bell. Designed with businesses of all sizes in mind, Xero offers wide accounting features to streamline accounting processes and empower users with real-time financial insights.

Xero has:

Like QuickBooks, it also operates on the cloud. It can be accessed on mobile devices as long as there is an internet connection.

For every small business owner, the ultimate goal is growth. If you envision managing a larger workforce and handling a growing client base, you can count on Sage.This tool has HR and CRM features that will be very helpful in managing your growing workforce.

These functionalities can effectively centralize and manage customer data, which is a big help for ecommerce sellers. This way, you can nurture stronger client relationships, track interactions, and identify opportunities for growth and upselling.

Sage has:

Many accounting software for small businesses pride themselves on being simple and user-friendly, and FreshBooks is one of them. The platform has been designed with the non-accountant in mind, offering intuitive features and a clean interface. Managing financial tasks is easy, making it accessible for entrepreneurs and small business owners.

FreshBooks has:

Wave Accounting is another addition to the user-friendly list. Its tagline flaunts that the tool was not made for accountants but for business owners themselves. Hence, its features are perfect for individuals with little bookkeeping and accounting knowledge. If you don’t have much time to learn the ropes of financial management, Wave Accounting is an excellent start.

Wave Accounting has:

You won’t be disappointed with Zoho Books. This free accounting software has superb customer service to help you establish and maintain your accounting and bookkeeping system.

Zoho Books has:

Now that you have all the essential information about top-notch bookkeeping software, you can check out which satisfies your business needs most to get the best.

If managing your startup's books proves daunting, Unloop is here to alleviate your burden. As one of the premier financial teams in North America, Unloop offers ecommerce services to go along with precise and detailed accounting.

Regardless of your sales channel—Amazon, Shopify, DTC, multichannel, or wholesale—we tailor our accounting services to your unique requirements. We can help you with the following:

Let’s discuss our offers further. Book a call now!

Disclaimer: Please note this article is not financial advice. The purpose of our blog is purely educational, so please consult a professional accountant or financial advisor before making any financial decision.

So you’ve started a small online business. You are now among the millions who have braved the ecommerce world. Since ecommerce is so complex, and the sheer volume of transactions can be intimidating, your accounting may need help to keep up with your online store. This is where choosing the best accounting software can be worth it.

Accounting software programs can do more than track the inflow and outflow of cash. You’ll be amazed at how they can be a one-stop shop for many of your digital needs, making them worthy of every penny you invest.

So, what’s the best small business accounting software for you? Find out all the answers here in this guide. But first, let’s talk about everything you need to know about ecommerce accounting.

Ecommerce is a worldwide business. In fact, Statista already presented compelling data, showing its global reach and exponential growth. Just think of the transactions that make up this figure—massive.

Given the wide reach, ecommerce accounting differs because there is so much more to account for. Take a look at some of them.

An online business can sell anywhere in the world through an ecommerce platform and exemplary shipping service. But to be able to sell legally, there must always be a sales tax attached to each sale.

Ecommerce accounting requires sales tax calculation for different tax policies. For example:

| Amazon can handle your taxes through Amazon Tax Exemption Program (ATEP) for sales in the US. But you'll still have to collect and remit your sales taxes in Canada. |

On top of that, the US and Canadian sales tax rates are completely different, with tax returns filed each year. Tax management is daunting, requiring careful attention and consideration.

Another thing that separates ecommerce from regular businesses is the vast inventory. Inventory tracking is no easy task for anybody, especially for small-scale startups. You need to have many products on-hand and ready to meet demand at a moment’s notice.

There will also be an inevitable addition to your accounting load, especially if you’re a business that ships to customers in different timezones. Add to that the sheer volume of items you’ll have to check on—where they are stored, how many are ready for shipping, how many are damaged or lost—and regularly reconcile in your records.

If you sell products or services worldwide, expect to see thousands of business transactions daily. That means various modes of payments, currencies, bank accounts, taxes, and so on.

Tracking each transaction will take copious amounts of time and energy. You might miss out on some financial data, which, for a global business, you cannot allow to happen.

While it's possible to do your accounting manually, tracing every ecommerce transaction can make even the best accountants dizzy. Giving your accounting specialist some much-needed assistance, like online accounting software, is recommended.

In addition to maximizing your time and resources, here are eight reasons accounting software is worth it for your small ecommerce business.

A bookkeeper can rely on accounting software to record transactions. Through it, they can take note of all business transactions involving money. They can ensure that income and expenses from different channels, like bank and credit cards or online payment gateways, are all accounted for.

Because of the high-tech tools available today, a bookkeeper’s task of typing data is slowly disappearing. Data from different sources can be connected to a central accounting system. There are also optical character recognition tools that minimize manual data entry.

Invoicing is an essential part of bookkeeping and accounts receivable management. Through software, you can conveniently send payment reminders to customers—all online. Simply schedule the sending date and time and let the software handle its transmission. If customers forget to pay, sending a nudge can also be done on the software.

Invoicing from an accounting tool also makes payment easier for customers as each invoice includes a “Pay Now” button. Customers can click on it for online payment. All money coming from this channel will automatically be recorded in the books.

The money you collect from customers and use to pay suppliers and expenses are all recorded in your business bank account. Through accounting software’s bank connection feature, you can have visibility on these transactions, and they will also be categorized into income and expenses in the books.

Bank reconciliation becomes a seamless process, as you can easily compare the details recorded in your books with the transactions listed in your bank statement. With this, you’ll be able to correct any mistakes and raise red flags on fraudulent deals.

Business planning and forecasting are vital as they allow you to see how your business will go in a projected period. It may not be 100% accurate, but you can still get the closest possible financial situation your business will see in the future.

Many accounting software has a feature that allows you to develop a business financial forecast in just a few clicks. Acquiring past and present numbers won’t be a problem as they are all recorded in the books.

Once you have the forecasted data, you can create plans based on numbers and even simulate results using the software. You can follow a strategy that gives you the best results from there.

The younger your business is, the more often you should generate financial reports. You must regularly check its financial health to adjust your strategies. Good financial reporting contains the following:

| Financial Reports | |

| Balance Sheet | Quickly check your assets, liabilities, and equity using this report. |

| Income Statement | Also known as the Profit and Loss Statement or Statement of Revenue and Expenses. This report shows your business's profit and how income and expenses impact it. |

| Cash Flow Statement | This report illustrates how money flows in and out of your business, showing your earnings and expenditures. |

| Statement of Owner’s Equity | For sole proprietors, this report displays earnings or profit and retained earnings. For corporations, it is referred to as Shareholder’s Equity. |

When you know these reports, you and your accountant can run and analyze them.

As mentioned earlier, inventory is a part of your company assets. You don’t want your customers disappointed because products are out of stock. This is where accounting software comes into play.

Accounting software isn’t only for numbers; it’s for your items too. When you can monitor your inventory, you’ll know which items fly off the shelves and which don’t move. You can also use the information to create plans to duplicate your successes and sell slow products.

Taxes are inevitable, but you can make them manageable. On top of calculation and collection, the best accounting software can handle tax remittance. You can integrate the data from these tools into your accounting system for tracking purposes.

Calculating your tax base and rate becomes easier regarding income tax returns, given the recorded income and expenses in the books. With the most comprehensive accounting software, tax season will be a breeze.

Ecommerce functions online. Data security and protection are indeed vital features you’ll look for in small business accounting programs. Luckily, online financial accounts are protected with cloud-based features.

Traditional accounting using Excel sheets stores books on computers. Still, cloud-based software has more advanced security features and can store information in the cloud. The cloud encrypts data, ensuring hackers and unauthorized individuals cannot access your accounting data. Corruption of data is also less likely.

Most cloud-based software have multiple users and role-based access, meaning only individuals you authorize can access the books.

Besides bookkeeping, inventory, cloud, and tax management, consider examining these features when selecting the most suitable accounting software solution for your business.

Any small business owner should have an accounts receivable feature in their software, given that payments are often made remotely with various payment schemes.

An accounts receivable lets you know how much money to expect and how much you can use to repurchase stock. It also tells you how much your business is shelling out weekly or monthly.

For example: If you're in the retail business, you may have scheduled shipments to replenish your inventory. Accounts payable notes this in advance for you to continue or change, depending on your decision.

Direct integration is also a crucial feature to look for in accounting software. It allows smooth alignment with the ecommerce platforms you've chosen for selling your products. The software can efficiently capture and organize all relevant accounting data by directly integrating with your online stores.

It also ensures that your accounting records are automatically updated in real time, reducing the risk of errors. With direct integration, you'll have an easier time keeping a thorough and accurate overview of your financial performance.

A mobile app functionality is a great feature to add to your accounting software. With everyone on the go nowadays, having a mobile app handy allows you and your staff to update your accounting whenever and wherever.

Being a startup, you can always pick the small business accounting software that can currently satisfy your financial management needs. But you must also choose the one that can scale to more advanced features as you grow your venture.

Here are popular accounting software ideal for ecommerce startups.

The most popular small business accounting software. It has all the features you need. When you sign up for a plan, it’ll backtrack all your financial transactions and do live bookkeeping moving forward.

QuickBooks has:

Xero is another accounting software that will surely ring a bell. Designed with businesses of all sizes in mind, Xero offers wide accounting features to streamline accounting processes and empower users with real-time financial insights.

Xero has:

Like QuickBooks, it also operates on the cloud. It can be accessed on mobile devices as long as there is an internet connection.

For every small business owner, the ultimate goal is growth. If you envision managing a larger workforce and handling a growing client base, you can count on Sage.This tool has HR and CRM features that will be very helpful in managing your growing workforce.

These functionalities can effectively centralize and manage customer data, which is a big help for ecommerce sellers. This way, you can nurture stronger client relationships, track interactions, and identify opportunities for growth and upselling.

Sage has:

Many accounting software for small businesses pride themselves on being simple and user-friendly, and FreshBooks is one of them. The platform has been designed with the non-accountant in mind, offering intuitive features and a clean interface. Managing financial tasks is easy, making it accessible for entrepreneurs and small business owners.

FreshBooks has:

Wave Accounting is another addition to the user-friendly list. Its tagline flaunts that the tool was not made for accountants but for business owners themselves. Hence, its features are perfect for individuals with little bookkeeping and accounting knowledge. If you don’t have much time to learn the ropes of financial management, Wave Accounting is an excellent start.

Wave Accounting has:

You won’t be disappointed with Zoho Books. This free accounting software has superb customer service to help you establish and maintain your accounting and bookkeeping system.

Zoho Books has:

Now that you have all the essential information about top-notch bookkeeping software, you can check out which satisfies your business needs most to get the best.

If managing your startup's books proves daunting, Unloop is here to alleviate your burden. As one of the premier financial teams in North America, Unloop offers ecommerce services to go along with precise and detailed accounting.

Regardless of your sales channel—Amazon, Shopify, DTC, multichannel, or wholesale—we tailor our accounting services to your unique requirements. We can help you with the following:

Let’s discuss our offers further. Book a call now!

Please note this article is not financial advice. The purpose of our blog is purely educational, so please consult a professional accountant or financial advisor before making any financial decision.

Any big or small business owner must ensure their employees receive the hard-earned money they deserve. Nevertheless, mistakes during payroll processing are bound to happen. Thankfully, the emergence of an automated payroll system allows you to pay your employees seamlessly.

Let's delve into the depths of an automated payroll solution and how it can transform your business’s financial operations.

Before we get into the nitty-gritty of payroll automation, it's crucial to understand the processes behind it. As you might have already guessed, payroll involves giving your employees accurate salaries on time.

To do so, you have to calculate

Additionally, you have to consider several other factors, such as

To any business owner without an established finance team, these tasks may become too confusing and daunting to handle on their own. Learning to do these accounting tasks accurately also takes much time and effort.

Fortunately, you won't have to stress too much over perfecting these tiresome payroll processes. With an automated payroll, you have an organized tool for the job. A computerized payroll system will simplify and speed up how you calculate and distribute your employee's paychecks.

An automated system can do the following processes:

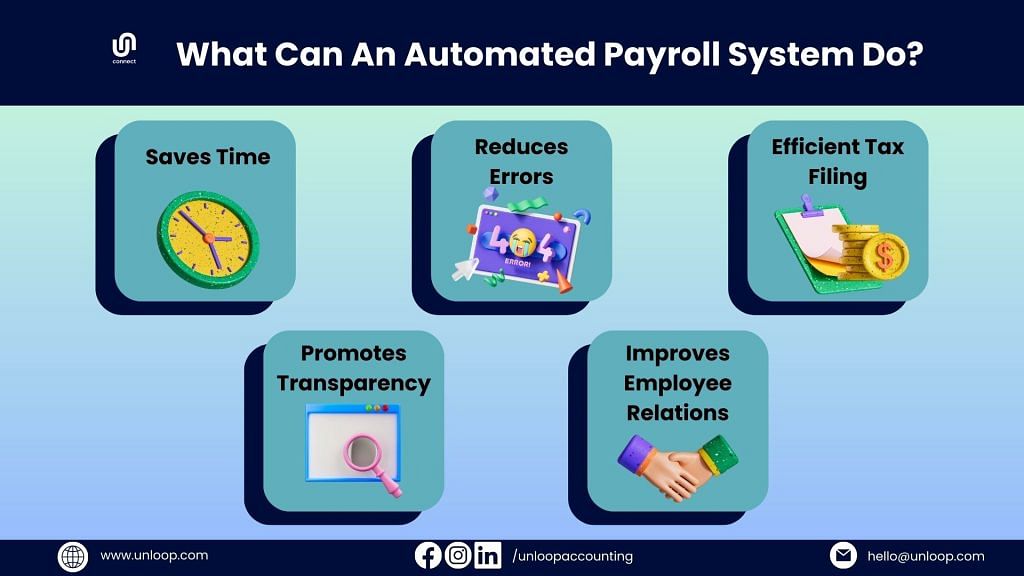

You might still be skeptical about streamlining your payroll tasks to organized software. To ease any of your worries, we've gathered a few reasons why you should automate payroll to improve your business.

Saves Time

Time is precious and should not be wasted. Even the tiniest moments count when you're operating and handling a business. Hence, it's only logical to spend every second wisely.

You would have to spend hours upon hours doing manual data entry for payroll when you should be working on important business matters. An automated payroll system allows you to allocate more time to those tasks.

Even the slightest mistake can cause grave consequences when calculating employee wages. The payroll team must ensure accurate and timely wage distribution.

However, with the dizzying amount of accounting and recordkeeping tasks involved in payroll, some people will inevitably make mistakes and unintentionally issue inaccurate employee payments. These errors can cause financial issues for both the employee and the employer and lead to severe legal penalties.

Precise and accurate payment calculations are guaranteed with a computerized payroll system. The software can correctly and swiftly compute and adjust an employee's pay while considering possible wage deductions, raises, bonuses, and more.

One of the most confusing and headache-inducing parts of payroll processing is filing and calculating tax withholdings. Getting this part right is crucial as it involves various laws and regulations. An error may likely result in legal trouble for your business.

With automated payroll systems, you don't have to calculate all of your employee's gross pay and take out tax deductions on your own. You can let the software accurately figure out and navigate the complicated world of tax filing.

Using automated payroll software can also foster employee trust. Most automated systems allow staff members to access their paychecks easily and view possible changes in their regular wages. These are possible with employee self-service portals and other employee-centric features.

They can also update and input payroll information easily using automated systems. Because of this feature, the system can smoothly adjust employee pay stubs according to real-time changes.

Paying employees with an automated system can indirectly improve your relationship with them. Receiving befitting compensation for their work is one of the primary ways to motivate employees. With computerized payroll systems, employees are guaranteed accurate and timely pay.

Moreover, with the transparency that automated systems provide, you can improve and develop trust and confidence in your employees. They will feel secure knowing that you pay them what they're due.

Manually handling your payroll may seem like a breeze at first. But as your business grows, it will become more complicated and time-consuming. The sooner you implement payroll automation, the more time and resources you'll save in the long run.

Hopefully, the benefits mentioned above are enough to convince you to start automating your payroll. Your next course of action is learning how to switch from manual to automated payroll. You can either use payroll automation software or hire a payroll service.

Take matters into your own hands by searching for payroll automation software that suits your business. Choosing payroll software will primarily depend on your company's size, business needs, and other related factors.

Besides the payroll software cost, here are some features you must consider:

Besides calculating your employee's wages, automated software can also provide regular comprehensive payroll reports to help monitor your finances. Some even use combined HR and payroll software for more efficient employee and payroll management.

Once you've made your choice, all you have to do is input the necessary payroll data and documents, such as employee information and tax forms, into the software. Ensure that what you've placed in the system is accurate to avoid financial errors.

Another option is to hire management assistance from professional payroll services. They especially come in handy for owners of large corporations and businesses handling a significant number of employees.

All you have to do is track your employees' work hours and forward this data to the service provider. The service will calculate the payroll amount based on those hours and deduct taxes from their paychecks before rolling them out during payday. Naturally, they would typically use automated software.

Payroll is part and parcel of any business, no matter the industry. Plenty of accounting tasks necessitate payroll processing, from tracking your employees' work hours to delivering their wages on time. While these tasks can be done independently and manually, doing so will be time-consuming and may lead to unintentional errors.

So, switch to stress-free automated payroll management with Unloop's payroll services. Our team of professionals uses efficient, up-to-date tools like QuickBooks to ensure automated, organized, and efficient payroll processing for your company. Book a call with us today!

Please note this article is not financial advice. The purpose of our blog is purely educational, so please consult a professional accountant or financial advisor before making any financial decision.

Any big or small business owner must ensure their employees receive the hard-earned money they deserve. Nevertheless, mistakes during payroll processing are bound to happen. Thankfully, the emergence of an automated payroll system allows you to pay your employees seamlessly.

Let's delve into the depths of an automated payroll solution and how it can transform your business’s financial operations.

Before we get into the nitty-gritty of payroll automation, it's crucial to understand the processes behind it. As you might have already guessed, payroll involves giving your employees accurate salaries on time.

To do so, you have to calculate

Additionally, you have to consider several other factors, such as

To any business owner without an established finance team, these tasks may become too confusing and daunting to handle on their own. Learning to do these accounting tasks accurately also takes much time and effort.

Fortunately, you won't have to stress too much over perfecting these tiresome payroll processes. With an automated payroll, you have an organized tool for the job. A computerized payroll system will simplify and speed up how you calculate and distribute your employee's paychecks.

An automated system can do the following processes:

You might still be skeptical about streamlining your payroll tasks to organized software. To ease any of your worries, we've gathered a few reasons why you should automate payroll to improve your business.

Saves Time

Time is precious and should not be wasted. Even the tiniest moments count when you're operating and handling a business. Hence, it's only logical to spend every second wisely.

You would have to spend hours upon hours doing manual data entry for payroll when you should be working on important business matters. An automated payroll system allows you to allocate more time to those tasks.

Even the slightest mistake can cause grave consequences when calculating employee wages. The payroll team must ensure accurate and timely wage distribution.

However, with the dizzying amount of accounting and recordkeeping tasks involved in payroll, some people will inevitably make mistakes and unintentionally issue inaccurate employee payments. These errors can cause financial issues for both the employee and the employer and lead to severe legal penalties.

Precise and accurate payment calculations are guaranteed with a computerized payroll system. The software can correctly and swiftly compute and adjust an employee's pay while considering possible wage deductions, raises, bonuses, and more.

One of the most confusing and headache-inducing parts of payroll processing is filing and calculating tax withholdings. Getting this part right is crucial as it involves various laws and regulations. An error may likely result in legal trouble for your business.

With automated payroll systems, you don't have to calculate all of your employee's gross pay and take out tax deductions on your own. You can let the software accurately figure out and navigate the complicated world of tax filing.

Using automated payroll software can also foster employee trust. Most automated systems allow staff members to access their paychecks easily and view possible changes in their regular wages. These are possible with employee self-service portals and other employee-centric features.

They can also update and input payroll information easily using automated systems. Because of this feature, the system can smoothly adjust employee pay stubs according to real-time changes.

Paying employees with an automated system can indirectly improve your relationship with them. Receiving befitting compensation for their work is one of the primary ways to motivate employees. With computerized payroll systems, employees are guaranteed accurate and timely pay.

Moreover, with the transparency that automated systems provide, you can improve and develop trust and confidence in your employees. They will feel secure knowing that you pay them what they're due.

Manually handling your payroll may seem like a breeze at first. But as your business grows, it will become more complicated and time-consuming. The sooner you implement payroll automation, the more time and resources you'll save in the long run.

Hopefully, the benefits mentioned above are enough to convince you to start automating your payroll. Your next course of action is learning how to switch from manual to automated payroll. You can either use payroll automation software or hire a payroll service.

Take matters into your own hands by searching for payroll automation software that suits your business. Choosing payroll software will primarily depend on your company's size, business needs, and other related factors.

Besides the payroll software cost, here are some features you must consider:

Besides calculating your employee's wages, automated software can also provide regular comprehensive payroll reports to help monitor your finances. Some even use combined HR and payroll software for more efficient employee and payroll management.

Once you've made your choice, all you have to do is input the necessary payroll data and documents, such as employee information and tax forms, into the software. Ensure that what you've placed in the system is accurate to avoid financial errors.

Another option is to hire management assistance from professional payroll services. They especially come in handy for owners of large corporations and businesses handling a significant number of employees.

All you have to do is track your employees' work hours and forward this data to the service provider. The service will calculate the payroll amount based on those hours and deduct taxes from their paychecks before rolling them out during payday. Naturally, they would typically use automated software.

Payroll is part and parcel of any business, no matter the industry. Plenty of accounting tasks necessitate payroll processing, from tracking your employees' work hours to delivering their wages on time. While these tasks can be done independently and manually, doing so will be time-consuming and may lead to unintentional errors.

So, switch to stress-free automated payroll management with Unloop's payroll services. Our team of professionals uses efficient, up-to-date tools like QuickBooks to ensure automated, organized, and efficient payroll processing for your company. Book a call with us today!

Learning how to calculate accounts receivable is an important step towards better financial management, and the reason is obvious for anyone that owns a business; nobody wants to forget the money they're owed, especially when it's a huge amount.

In this blog, we'll discuss everything there is to know about accounts receivable, the formulas involved in calculating it, and why you need to keep tabs on this account that's on your company's balance sheet.

For starters, let's discuss what accounts receivable is. The short of it is that it's the money that customers owe a business on credit. But how does that happen exactly?

Accounts receivable are recorded on the business's books when a customer receives goods or services from the business but can't pay at the time of purchase.

For example, an Amazon seller may provide products to a client and invoice them for the products. If the client does not pay immediately, the amount owed by the client for the products is recorded as an accounts receivable.

Accounts receivable can also be accrued through installment payments or financing arrangements, such as when a customer purchases a product on credit and pays for it over time.

During the pandemic, many businesses learned that proper accounts receivable management can lead to sturdy financial positions. You see, accruing accounts receivable allows businesses to provide flexibility to their customers while still being able to track and manage the money owed to them.

Owing money can also work both ways. With accounts receivable, a business is owed by its customers for every product or service it sells on credit. Accounts payable is the opposite. It happens when the business owes its vendors or suppliers money for goods or services received but has yet to pay for them.

On the balance sheet, both accounts are recorded differently. Accounts receivable are recorded as assets, while accounts payable are considered liabilities.

A good balance between accounts receivable and accounts payable is critical for maintaining a healthy cash flow and financial stability.

Accounts receivable is only recognized as an asset when a business has a legal right to receive payment from a customer for goods or services that have been provided but not yet paid for.

Accounts receivable are classified as a current asset because it is expected to be collected relatively quickly, typically within 30 to 60 days. As such, accounts receivable represent an essential component of a business's overall financial health, as it reflects the amount of cash the business expects to receive soon.

Under the cash basis accounting method, accounts receivable are only recorded once payment is received. Any sales made on credit or outstanding invoices are recorded as revenue once the payment is received. Hence, the accounts receivable balance remains zero until the customer pays.

On the other hand, under the accrual accounting method, accounts receivable are recorded as soon as the sale is made or the service is provided, even if payment has yet to be received. This means that the revenue is recognized at the time of the sale or service, regardless of when payment is received. The accounts receivable balance reflects the total amount owed by customers as of the end of the reporting period.

So how do you calculate accounts receivable? Do you rely on accounting software to handle everything financial-related? Do you hire an accountant to deal with the math?

The truth is, it's best if new business owners like yourself understand how it's calculated to better maneuver net sales and other essential accounts in your day-to-day transactions.

Currently, there are two standard methods for accounts receivable calculation: the balance sheet method and the aging method.

The balance sheet method involves taking the total accounts receivable balance on the balance sheet and subtracting any allowances for doubtful accounts.

The allowance for doubtful accounts is an estimated amount of uncollectible debts based on experience or other factors. The result is the net accounts receivable balance, which represents the amount the business expects to collect from its customers.

Accounts Receivable (AR) - Allowance for Doubtful Accounts (ADA) = Net Accounts Receivable (NAR)

The aging method involves categorizing the accounts receivable by the age of the invoice or outstanding payment. Typically, businesses will group the accounts receivable in 30-day intervals, such as current, 1–30 days, 31–60 days, and so on.

For each age category, the business estimates the percentage of the outstanding balance likely to be collected. This percentage is based on historical data or industry averages. The sum of the estimated amounts for each age category is the total estimated accounts receivable balance.

(Amounts outstanding up to 30 days × Estimated percentage collectible) + (Amounts outstanding 31–60 days × Estimated percentage collectible) + (Amounts outstanding 61–90 days × Estimated percentage collectible) + (Amounts outstanding over 90 days × Estimated percentage collectible) = Total estimated accounts receivables

The balance sheet method is simple and quick but provides less detailed information on the accounts receivable than the aging method.

The aging method takes more time and effort to calculate, but it provides a more detailed breakdown of the accounts receivable by age, which can help determine which invoices are most overdue and require immediate attention.

Ultimately, businesses should choose the best method for their needs and resources.

Analyzing accounts receivable is vital for cash flow, financial planning, and risk management. It allows businesses to identify areas where they may be experiencing delays in payment or facing issues with collection, enabling them to take corrective action and improve their cash flow.

By understanding the trends and patterns in their accounts receivable, businesses can make more accurate financial projections and plan for future growth.

Now, there are several metrics that businesses can use to analyze accounts receivable. Here are some of the most commonly used ones.

This ratio measures how often a business collects its average accounts receivable balance during a given period. The accounts receivable turnover ratio formula is:

Accounts Receivable Turnover Ratio = Net Credit Sales / Average Accounts Receivable

A high ratio indicates that the business is collecting its receivables in a timely manner, while a low ratio indicates that the business is taking a long time to collect its receivables or needs a better collection process.

DSO measures the average number of days it takes for a business to collect payment on its sales. The formula for DSO is:

DSO = (Accounts Receivable / Net Credit Sales) x Number of Days in the Period

Unlike the accounts receivable turnover ratio, a lower DSO indicates that a business collects payment more quickly. In comparison, a higher DSO indicates that the business is taking longer to collect a payment, which can lead to cash flow problems and may require additional efforts to improve the accounts receivable collection process.

This ratio measures the percentage of accounts receivable the business writes off as bad debt. The formula is:

Bad Debt Ratio = (Total Bad Debts / Net Credit Sales) x 100

A lower lousy debt ratio indicates that the business effectively manages its accounts receivable and minimizes the risk of bad debts.

This metric measures the average number of days it takes for a business to collect payment on its accounts receivable. The formula is:

Average Collection Period = (Accounts Receivable / Net Credit Sales) x Number of Days in the Period

A lower average collection period indicates that the business is collecting payment more quickly, while a higher average collection period indicates the business is taking a long time to collect payment.

In the same way that we ought to calculate accounts receivable accurately, we want to be sure that we're managing collections responsibly. The goal is always to what your company collects so we can avoid future financial difficulties and maximize the company's ability to generate revenue.

To better manage your accounts receivables, here are a few tips that can help:

In conclusion, calculating and managing accounts receivable is critical to a business's financial health. It is important to regularly analyze accounts receivable, identify issues, and implement effective strategies to manage them.

At Unloop, we understand that and want to ensure you succeed.

By working with our accounting experts, you can focus on running your business while we handle your accounting needs, ensuring that your business stays on track and financially healthy—we’ve even got accounts payable services!

Contact us today to learn how we can help you manage your accounts receivable and achieve financial success.

Learning how to calculate accounts receivable is an important step towards better financial management, and the reason is obvious for anyone that owns a business; nobody wants to forget the money they're owed, especially when it's a huge amount.

In this blog, we'll discuss everything there is to know about accounts receivable, the formulas involved in calculating it, and why you need to keep tabs on this account that's on your company's balance sheet.

For starters, let's discuss what accounts receivable is. The short of it is that it's the money that customers owe a business on credit. But how does that happen exactly?

Accounts receivable are recorded on the business's books when a customer receives goods or services from the business but can't pay at the time of purchase.

For example, an Amazon seller may provide products to a client and invoice them for the products. If the client does not pay immediately, the amount owed by the client for the products is recorded as an accounts receivable.

Accounts receivable can also be accrued through installment payments or financing arrangements, such as when a customer purchases a product on credit and pays for it over time.

During the pandemic, many businesses learned that proper accounts receivable management can lead to sturdy financial positions. You see, accruing accounts receivable allows businesses to provide flexibility to their customers while still being able to track and manage the money owed to them.

Owing money can also work both ways. With accounts receivable, a business is owed by its customers for every product or service it sells on credit. Accounts payable is the opposite. It happens when the business owes its vendors or suppliers money for goods or services received but has yet to pay for them.

On the balance sheet, both accounts are recorded differently. Accounts receivable are recorded as assets, while accounts payable are considered liabilities.

A good balance between accounts receivable and accounts payable is critical for maintaining a healthy cash flow and financial stability.

Accounts receivable is only recognized as an asset when a business has a legal right to receive payment from a customer for goods or services that have been provided but not yet paid for.

Accounts receivable are classified as a current asset because it is expected to be collected relatively quickly, typically within 30 to 60 days. As such, accounts receivable represent an essential component of a business's overall financial health, as it reflects the amount of cash the business expects to receive soon.

Under the cash basis accounting method, accounts receivable are only recorded once payment is received. Any sales made on credit or outstanding invoices are recorded as revenue once the payment is received. Hence, the accounts receivable balance remains zero until the customer pays.

On the other hand, under the accrual accounting method, accounts receivable are recorded as soon as the sale is made or the service is provided, even if payment has yet to be received. This means that the revenue is recognized at the time of the sale or service, regardless of when payment is received. The accounts receivable balance reflects the total amount owed by customers as of the end of the reporting period.

So how do you calculate accounts receivable? Do you rely on accounting software to handle everything financial-related? Do you hire an accountant to deal with the math?

The truth is, it's best if new business owners like yourself understand how it's calculated to better maneuver net sales and other essential accounts in your day-to-day transactions.

Currently, there are two standard methods for accounts receivable calculation: the balance sheet method and the aging method.

The balance sheet method involves taking the total accounts receivable balance on the balance sheet and subtracting any allowances for doubtful accounts.

The allowance for doubtful accounts is an estimated amount of uncollectible debts based on experience or other factors. The result is the net accounts receivable balance, which represents the amount the business expects to collect from its customers.

Accounts Receivable (AR) - Allowance for Doubtful Accounts (ADA) = Net Accounts Receivable (NAR)

The aging method involves categorizing the accounts receivable by the age of the invoice or outstanding payment. Typically, businesses will group the accounts receivable in 30-day intervals, such as current, 1–30 days, 31–60 days, and so on.

For each age category, the business estimates the percentage of the outstanding balance likely to be collected. This percentage is based on historical data or industry averages. The sum of the estimated amounts for each age category is the total estimated accounts receivable balance.

(Amounts outstanding up to 30 days × Estimated percentage collectible) + (Amounts outstanding 31–60 days × Estimated percentage collectible) + (Amounts outstanding 61–90 days × Estimated percentage collectible) + (Amounts outstanding over 90 days × Estimated percentage collectible) = Total estimated accounts receivables

The balance sheet method is simple and quick but provides less detailed information on the accounts receivable than the aging method.

The aging method takes more time and effort to calculate, but it provides a more detailed breakdown of the accounts receivable by age, which can help determine which invoices are most overdue and require immediate attention.

Ultimately, businesses should choose the best method for their needs and resources.

Analyzing accounts receivable is vital for cash flow, financial planning, and risk management. It allows businesses to identify areas where they may be experiencing delays in payment or facing issues with collection, enabling them to take corrective action and improve their cash flow.

By understanding the trends and patterns in their accounts receivable, businesses can make more accurate financial projections and plan for future growth.

Now, there are several metrics that businesses can use to analyze accounts receivable. Here are some of the most commonly used ones.

This ratio measures how often a business collects its average accounts receivable balance during a given period. The accounts receivable turnover ratio formula is:

Accounts Receivable Turnover Ratio = Net Credit Sales / Average Accounts Receivable

A high ratio indicates that the business is collecting its receivables in a timely manner, while a low ratio indicates that the business is taking a long time to collect its receivables or needs a better collection process.

DSO measures the average number of days it takes for a business to collect payment on its sales. The formula for DSO is:

DSO = (Accounts Receivable / Net Credit Sales) x Number of Days in the Period

Unlike the accounts receivable turnover ratio, a lower DSO indicates that a business collects payment more quickly. In comparison, a higher DSO indicates that the business is taking longer to collect a payment, which can lead to cash flow problems and may require additional efforts to improve the accounts receivable collection process.

This ratio measures the percentage of accounts receivable the business writes off as bad debt. The formula is:

Bad Debt Ratio = (Total Bad Debts / Net Credit Sales) x 100

A lower lousy debt ratio indicates that the business effectively manages its accounts receivable and minimizes the risk of bad debts.

This metric measures the average number of days it takes for a business to collect payment on its accounts receivable. The formula is:

Average Collection Period = (Accounts Receivable / Net Credit Sales) x Number of Days in the Period

A lower average collection period indicates that the business is collecting payment more quickly, while a higher average collection period indicates the business is taking a long time to collect payment.

In the same way that we ought to calculate accounts receivable accurately, we want to be sure that we're managing collections responsibly. The goal is always to what your company collects so we can avoid future financial difficulties and maximize the company's ability to generate revenue.

To better manage your accounts receivables, here are a few tips that can help:

In conclusion, calculating and managing accounts receivable is critical to a business's financial health. It is important to regularly analyze accounts receivable, identify issues, and implement effective strategies to manage them.

At Unloop, we understand that and want to ensure you succeed.

By working with our accounting experts, you can focus on running your business while we handle your accounting needs, ensuring that your business stays on track and financially healthy—we’ve even got accounts payable services!

Contact us today to learn how we can help you manage your accounts receivable and achieve financial success.

Amazon has revolutionized the shopping process for both large and small businesses. Selling your products online allows your business to expose your products to millions of customers. However, since online selling is continuing to be popular with entrepreneurs, you also have millions of competitors out there.

If you are determined to put your business online, Amazon is the best for you. Setting up an Amazon Business account helps companies get ahead by giving Amazon-exclusive discounts on pricing, plus it offers features to aid in your business operations.

Amazon Business is a business-focused account that caters to all businesses, from small and medium to large enterprises. The main purpose of a business account is for businesses to have an approval process so they can keep their spending in check.

Business accounts allow an entity to create multiple users to make purchases for the company. Your business also enjoys the benefits of efficient and swift deliveries. But, it doesn’t stop there! Once you have a business account, you can upgrade to a Prime account which opens your business to more exclusive benefits.

But unlike business accounts (which are free), Prime members need to pay a membership fee to enjoy its features.

Amazon Prime membership fees may vary depending on the number of users that use the account. Here is a breakdown of their annual prices.

| Number of Users | 1 user | 3 users | 10 users | 100 users | Unlimited Users |

| Price | $69 | $179 | $499 | $1,299 | $10,099 |

You may be thinking that you already have a personal account, So why do you still need to get a Business account? Amazon offers many features and services exclusive to business account holders. For example, having these accounts opens you to business-only selections, bulk discounts, and a wide variety of product lines.

Once your Amazon Business account is set up, you can add multiple sellers in one central account, which anyone in your business can use. The benefits of an Amazon business account is for both the seller and buyer, and here's what you can do with it.

Amazon helps with the selling process when you set up a business account, and it's free. Whether you're a small-scale one-person business or a larger enterprise, it doesn't matter. Any company can open a business account.

To set up your account:

There are over 5 million products currently available across business accounts on Amazon. Aside from access to an unlimited number of items, you also enjoy exclusive prices for business account holders. Whether you do B2B transactions or use your business account as a buyer, you'll enjoy discounts that are not available on personal accounts.

Amazon offers lower prices for bulk purchases. Furthermore, you can ask sellers for discounts.

In 2022, there were currently 200 million active users on Amazon. This number grows each year. When you enroll in Amazon Business, your products will be listed in the vast Amazon catalog, which is accessible to millions of established customers.

Whether you sell from the US or are an international seller, you will be eligible for the FBA program. Amazon is available in numerous countries worldwide, and is continually expanding. Amazon has warehouses in different locations even outside of the US, so international sellers can enjoy the FBA program too.

Furthermore, since the primary feature of FBA is storing your products and shipping, you can save money from renting warehouse space and hiring extra workers for the shipping and packing process. You can also guarantee that the FBA program will handle your products correctly to satisfy your customers.

You can choose to upgrade to a Business Prime account if you already have a Business account. The Prime account is a membership offered by Amazon for businesses and companies. Using a Business Prime account comes with more benefits compared to a standard business account. However, Amazon charges businesses when they upgrade to Prime depending on the number of users in your account.

So is it worth upgrading to a Business Prime account? Here are a few benefits of Amazon Business Prime memberships.

With a Prime account, you can send orders to your customers faster. Customers who shop from your business can enjoy discounted shipping rates, and even free one- or two-day shipping on eligible items. Free shipping will entice shoppers to buy from your business primarily because of the savings they can get.

Free Survey and Analytics Tool

It's vital for businesses to know the feedback of their customers regarding their products and services. Amazon helps companies gather their customer's reviews by using a third-party application. The free tool Amazon provides sends surveys to your customers via SMS, emails, POS kiosks, and other integrated services.

The free analytics tool is beneficial for businesses to track their growth, and with Amazon Prime, you get to enjoy these tools for free.

You will receive an Amazon Business American Express card upon membership with Amazon Prime. This card is exclusive to Prime holders and has no annual fees. With the card, you can enjoy 5% cashback or 90 days to pay with no interest for your purchases.

Amazon Workdocs allows you to store your essential business files in one location. You can quickly locate invoices, receipts, and other documents, allowing for collaborations.

The guided buying allows you to create buying policies for your Business Prime account.

If you have staff, you might give them the responsibility of making purchases from other companies. You can control the items they buy through the guided buying feature. You can list approved items they can purchase and put up restricted categories.

If there's a way to make selling on Amazon better and more convenient, grab it. Utilize the advantages of having an Amazon Business account. If you have the budget for a Business Prime membership, you're in for more benefits and tons of savings for your business. So don't forget to sign your business up today.

Running a small ecommerce firm may also be time-consuming and labour-intensive. While you handle selling your products and launching advertisements, Unloop can help with the accounting side of things. Unloop can help your business stay on top of taxes, expenses, payroll, and several other accounting tasks.

Book a call with us and learn more about how to get started.

Amazon has revolutionized the shopping process for both large and small businesses. Selling your products online allows your business to expose your products to millions of customers. However, since online selling is continuing to be popular with entrepreneurs, you also have millions of competitors out there.

If you are determined to put your business online, Amazon is the best for you. Setting up an Amazon Business account helps companies get ahead by giving Amazon-exclusive discounts on pricing, plus it offers features to aid in your business operations.

Amazon Business is a business-focused account that caters to all businesses, from small and medium to large enterprises. The main purpose of a business account is for businesses to have an approval process so they can keep their spending in check.

Business accounts allow an entity to create multiple users to make purchases for the company. Your business also enjoys the benefits of efficient and swift deliveries. But, it doesn’t stop there! Once you have a business account, you can upgrade to a Prime account which opens your business to more exclusive benefits.

But unlike business accounts (which are free), Prime members need to pay a membership fee to enjoy its features.

Amazon Prime membership fees may vary depending on the number of users that use the account. Here is a breakdown of their annual prices.

| Number of Users | 1 user | 3 users | 10 users | 100 users | Unlimited Users |

| Price | $69 | $179 | $499 | $1,299 | $10,099 |

You may be thinking that you already have a personal account, So why do you still need to get a Business account? Amazon offers many features and services exclusive to business account holders. For example, having these accounts opens you to business-only selections, bulk discounts, and a wide variety of product lines.

Once your Amazon Business account is set up, you can add multiple sellers in one central account, which anyone in your business can use. The benefits of an Amazon business account is for both the seller and buyer, and here's what you can do with it.

Amazon helps with the selling process when you set up a business account, and it's free. Whether you're a small-scale one-person business or a larger enterprise, it doesn't matter. Any company can open a business account.

To set up your account:

There are over 5 million products currently available across business accounts on Amazon. Aside from access to an unlimited number of items, you also enjoy exclusive prices for business account holders. Whether you do B2B transactions or use your business account as a buyer, you'll enjoy discounts that are not available on personal accounts.

Amazon offers lower prices for bulk purchases. Furthermore, you can ask sellers for discounts.

In 2022, there were currently 200 million active users on Amazon. This number grows each year. When you enroll in Amazon Business, your products will be listed in the vast Amazon catalog, which is accessible to millions of established customers.

Whether you sell from the US or are an international seller, you will be eligible for the FBA program. Amazon is available in numerous countries worldwide, and is continually expanding. Amazon has warehouses in different locations even outside of the US, so international sellers can enjoy the FBA program too.

Furthermore, since the primary feature of FBA is storing your products and shipping, you can save money from renting warehouse space and hiring extra workers for the shipping and packing process. You can also guarantee that the FBA program will handle your products correctly to satisfy your customers.

You can choose to upgrade to a Business Prime account if you already have a Business account. The Prime account is a membership offered by Amazon for businesses and companies. Using a Business Prime account comes with more benefits compared to a standard business account. However, Amazon charges businesses when they upgrade to Prime depending on the number of users in your account.

So is it worth upgrading to a Business Prime account? Here are a few benefits of Amazon Business Prime memberships.

With a Prime account, you can send orders to your customers faster. Customers who shop from your business can enjoy discounted shipping rates, and even free one- or two-day shipping on eligible items. Free shipping will entice shoppers to buy from your business primarily because of the savings they can get.

Free Survey and Analytics Tool

It's vital for businesses to know the feedback of their customers regarding their products and services. Amazon helps companies gather their customer's reviews by using a third-party application. The free tool Amazon provides sends surveys to your customers via SMS, emails, POS kiosks, and other integrated services.

The free analytics tool is beneficial for businesses to track their growth, and with Amazon Prime, you get to enjoy these tools for free.

You will receive an Amazon Business American Express card upon membership with Amazon Prime. This card is exclusive to Prime holders and has no annual fees. With the card, you can enjoy 5% cashback or 90 days to pay with no interest for your purchases.

Amazon Workdocs allows you to store your essential business files in one location. You can quickly locate invoices, receipts, and other documents, allowing for collaborations.

The guided buying allows you to create buying policies for your Business Prime account.

If you have staff, you might give them the responsibility of making purchases from other companies. You can control the items they buy through the guided buying feature. You can list approved items they can purchase and put up restricted categories.

If there's a way to make selling on Amazon better and more convenient, grab it. Utilize the advantages of having an Amazon Business account. If you have the budget for a Business Prime membership, you're in for more benefits and tons of savings for your business. So don't forget to sign your business up today.

Running a small ecommerce firm may also be time-consuming and labour-intensive. While you handle selling your products and launching advertisements, Unloop can help with the accounting side of things. Unloop can help your business stay on top of taxes, expenses, payroll, and several other accounting tasks.

Book a call with us and learn more about how to get started.

Trading in your Windows-based accounting system for Apple accounting software can be daunting at first. It often requires a significant adjustment in how you oversee financial operations. You might also feel like the new application holds your potential back, leaving you stuck and frustrated.

Don’t worry! The switch may have its challenges, but it also offers exciting opportunities. There is now free accounting software specifically made for your current setup.

Start your accounting journey on the right foot with these tips for finding the right software solution designed for Mac users. Get ready to streamline and facilitate every financial aspect of running a small business.

Apple is committed to revolutionizing the business world by introducing cutting-edge features such as accounting into its operating system. They aim to simplify digital operations for enterprises and open up more opportunities that provide maximum return on investment, freeing them from compatibility problems.

Thanks to Mac-friendly accounting software, entrepreneurs everywhere can experience an exponential increase in productivity and workflows. No longer should they miss out on the huge gains of modern financial programs—software is a must-have for new Apple users who want to continue their business efficiency.

Financial statements and graph visualizations are also taken to a whole new level when using accounting software for Mac. Every table and chart a business produces showcases its best work like never before. They can even present data points without sacrificing quality.

Best of all, small business owners won't have to worry about inaccuracies that come with manually handling accounts. Like with Windows, software is automated and adaptive for Mac users everywhere.

All these factors make software an ideal solution for successful financial collaborations.

With the overwhelming variety of Mac accounting software programs, it can be challenging to choose just one. But you’ll soon discover the best accounting software for your accounting needs by considering certain key factors in your decision-making process.

Here are a few things to keep in mind.

The availability of both online and offline versions is a great starting point for your research. With cloud-based accounting software, you can get vital information from any corner, making financial processes much more manageable.

At the same time, going offline provides users with secure access free of connection errors or other technical trouble. Users can take full advantage of their informational needs and wants by having both options available.

There may be times when you’ll need to move your financial data from your Mac computer to other Apple devices such as iPads or iPhones. This extra feature can make transferring and syncing records much more accessible and smoother.

By staying connected with your accounts, you can ensure that no important update or deadline slips past unnoticed. It may be a low priority for some, but getting an iOS app can make a difference in terms of convenience.

Don't get bogged down with payroll calculations; choose an accounting software solution for your Mac desktop with integrated payroll management tools. With this feature, you can easily access employee data analytics and calculate salaries to help you breeze through those operations.

Payroll integration guarantees timely tax withholdings, employee payments, and federal and state regulations compliance. Automating these business processes improves bookkeeping tasks and offers an extra layer of assurance and peace of mind.

Keep your Mac desktop running with accounting software that includes automatic reconciliation features. As the name suggests, it allows small businesses to manage monthly transactions without the time-consuming hassle of data entry and manual reconciliations.

Automated reconciliation can verify bank accounts, credit cards, and other transactions within the accounting system against their sources. From there, users can gain insight into company finances—all in a fraction of the usual processing period.

Finding an accounting platform with unlimited user access is ideal for effective operation and future growth so your team can thrive without additional financial burdens.

Companies can control their data and collaboration efforts with unlimited access to a single account. These accounting software features also have major implications for tracking employee productivity. Integrating this with team management tools means they can maximize efficiency in their accounting tasks like never before.

For Mac desktop users, customer support is an often ignored yet fundamental element when choosing the perfect accounting software. Eye-catching interfaces and tech enhancements may be a plus, but strong customer support can address any issues or queries you may have—proving why this feature shouldn't go unnoticed.

Poor customer service can leave you feeling stranded and frustrated. Make sure your digital experience is worry-free by selecting an accounting solution that delivers reliable, patient, and knowledgeable support when dealing with account-related matters.

Good accounting software should give you easy access to the customer-facing aspects of your financials, such as professional invoices, purchase order management, and customer accounts. This way, you can prepare for conversations with clients and vendors.

Leveraging an integrated client data system can also open a world of market access. It makes it easier to manage emails, conduct follow-up interactions with customers, get an overview of the customer journey, and make data-driven decisions that propel your enterprise forward.

Here’s your chance to be resourceful without sacrificing productivity. Accounting software with excellent expense tracking, reporting capabilities, and tax calculation is much-need for any business.

You can’t go wrong with these accounting features to easily manage hundreds of transactions and sort them out quickly. By finding a way to accurately break down expenses, measure necessary data research, and initiate automated calculations, you can access any information related to expenses without intricacy.

It’s time to move on to the next step—finding the right accounting programs for your device. With all the knowledge you need, you can dive into some of the excellent options available from Apple.

Below are the best accounting solutions for Apple’s operating system. From the highly advanced to simple, user-friendly tools, there’s sure to be an accounting app that fits what you’re looking for.

QuickBooks Online is the go-to choice for small business owners looking to control their money operations. This cloud accounting software empowers entrepreneurs with features like invoice tracking, expense monitoring, and secure payment acceptance, enabling them to stay on top of their finances without inconvenience.

Another version of QuickBooks is available to many Mac Users: QuickBooks Desktop App for Mac. It can give you instant insight into cash flow and profitability. It can also link directly to bank accounts, so you don't have to load multiple financial applications. Unfortunately, you can no longer enjoy this version after May 2023. So use it while you can.

FreshBooks is another small business accounting software option for Apple. From tracking billable hours to safeguarding data integrity in the cloud, this tool offers an Apple-friendly approach to tackling all your monetary resources.

With FreshBooks, companies can trust that their accounting operations have powerful capabilities to monitor and evaluate expenses. This gives an unbeatable view of its return on investment while categorizing personal and business finances.

Sage's basic subscription offers the perfect starting point for small business owners who want to get their finances in order. Accounting and organizational tools give users a helping hand to focus on growing their business without worrying about numbers or clutter.

With its intuitive interface, 1-on-1 expert session, and secure payment processing options, this scalable accounting software is setting a new benchmark in the field, proving to be an invaluable asset for any Mac user.

Xero is the perfect pick for taking care of those pesky accounting tasks. With clear interfaces and convenient features like capturing snapshots of key accounts, you can easily reference previous versions with one click, making it perfect for even the busiest business owner.

Xero also can add additional users to their plan without increased cost. It is perfect for companies with multiple staff involved in their accounting processes. Apple users no longer have to strain over the paperwork. Instead, they can keep things efficient and organized.