Are there moments you find yourself asking, “How often should you reconcile your bank account?”

Bank account reconciliation is an essential practice for maintaining financial accuracy and ensuring timely reporting. The task involves comparing your business's accounting records to your bank statement, identifying any discrepancies, and making necessary adjustments.

Through bank account reconciliation, you are sure that your financial records are accurate. Regularly reconciling your bank account not only helps to identify potential errors or fraudulent activity but also provides insight into your company's cash flow. By staying on top of these reconciliations, you can confidently make informed decisions.

With these, let us know the appropriate frequency for reconciling your bank account to achieve your goals and the benefits that come with it.

Bank reconciliation should be done on a regular basis, preferably monthly or quarterly, to ensure accuracy between bank statements and accounting records and to detect any discrepancies or errors.

To help you decide better on how often you should do your business bank reconciliation, let us go through the benefits of the different schedules and the process in doing them.

Performing weekly bank reconciliations can help you maintain up-to-date financial records and monitor your cash flow effectively. By reconciling your bank account and books weekly, you can spot any discrepancies or potential fraud early on, allowing for swift resolution.

Weekly reconciliation assists you in managing your cash account and accounts receivable more effectively, avoiding overdraft fees, and ensuring sufficient funds for accounts payable.

To perform a weekly reconciliation, have a daily balance sheet and bank statement comparison. Identify and resolve any discrepancies, such as bank errors, adjusting journal entries, or unusual transactions. Reconcile each transaction individually to ensure accuracy.

Monthly reconciliation is crucial for tracking and controlling your business's cash flow and financial health. Banks typically send monthly statements for the previous month, making it essential to reconcile your books and bank balance regularly. By performing a monthly reconciliation, you can catch any missed payments, double payments, or accounting errors.

Focus on your daily and weekly cash account balance, and compare it with the bank statement balance. Make sure that outstanding checks, deposits in transit, bank charges, and interest income are all included in the details. If you find any discrepancies, make any necessary adjustments to journal entries or correct calculation errors for accuracy.

Conducting quarterly or annual reconciliations provides an opportunity to review your financial records comprehensively, identifying any possible fraud or accounting errors that may have gone unnoticed during the weekly and monthly processes.

A more in-depth review of your financial records at the end of a quarter or fiscal year allows for a thorough analysis of your cash accounts, accounts payable, and accounts receivable.

Compile the bank statements for the entire quarter or year and compare them with your cash account and general ledger. Review the bank accounts for any unexplained transactions or discrepancies not identified during the weekly or monthly reconciliations. Make any necessary adjusting journal entries to correct discrepancies.

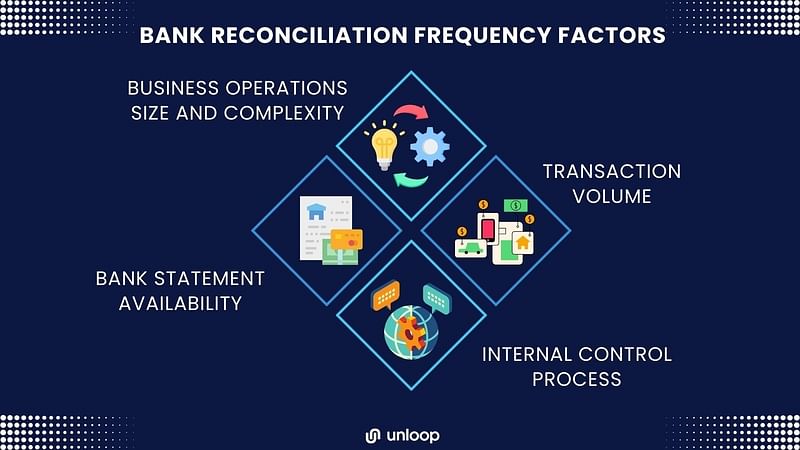

When considering how often to reconcile your bank account, consider the factors below too. These details can influence the best frequency for timely and accurate financial reporting.

Larger businesses with more complex operations may need to reconcile their bank accounts more frequently, as they are likely to have more transactions and a higher risk of fraud or accounting errors. Smaller businesses with fewer transactions, on the other hand, may be able to perform bank reconciliations less frequently, such as on a monthly basis, without sacrificing the accuracy of their financial reporting.

A higher volume of transactions can lead to more potential discrepancies between your cash account and your bank statement. Therefore, if your business has a high volume of transactions, it may be more efficient and accurate to reconcile your bank account more frequently, such as weekly or even daily. Conversely, businesses with lower transaction volumes might find it sufficient to reconcile their accounts on a monthly basis.

The frequency at which your bank provides statements will also influence reconciliation prevalence. Typically, banks send monthly statements, which aligns well with a monthly reconciliation schedule. However, with online banking and access to daily transaction updates, you may choose to reconcile your account more frequently to stay on top of your financial records.

The strength of your internal control processes will play a role in bank reconciliation frequency. Segregation of duties and a thorough review process will allow for timely identification and resolution of discrepancies. You can minimize the risk of fraud and accounting errors whether you choose to reconcile your bank account daily, weekly, or monthly.

Reconciling your bank account regularly for timely and accurate financial reporting will be easier with the various software available. The tools below can help streamline your bank reconciliation process to improve efficiency and reduce errors.

You cannot miss QuickBooks in accounting. This tool offers features for reconciling bank accounts and credit card transactions, making it easier for you to identify discrepancies in your financial records and keeping financial data correct and updated.

Another accounting software that can assist in your reconciliation process is Xero. Xero provides tools for bank reconciliation, allowing you to efficiently track and match transactions. Its bank feed feature also reduces manual effort and increases accuracy.

Sage Intacct offers automated bank reconciliation capabilities. This cloud-based accounting tool helps you streamline the process and identify bank errors or discrepancies in your financial records quickly and efficiently.

BlackLine Account Reconciliation is an enterprise-grade solution that enables users to streamline the reconciliation process, improve productivity, and ensure accuracy.

ReconArt is a comprehensive reconciliation software that provides a unified platform for performing reconciliations across various accounts and sources.

FloQast is an accounting workflow automation platform that includes reconciliation capabilities, facilitating collaboration and ensuring accuracy during the process.

SAP S/4HANA is an integrated enterprise resource planning (ERP) system that includes built-in reconciliation functionality, minimizing manual effort and maximizing efficiency.

By now, you already have an idea on how often you should do your bank reconciliation for your business. But before you get going check out these mistakes and challenges first. By being aware of these common mistakes and challenges, you can ensure a more timely and accurate bank reconciliation process.

Bank account reconciliation is essential for maintaining accurate financial records and identifying discrepancies before they escalate. By reconciling your accounts on a regular basis, you can ensure the integrity of your cash flow and make informed financial decisions.

For seamless bookkeeping and expert assistance with bank reconciliations, consider partnering with us here Unloop. With our range of financial services, from accounts payable, payroll, and tax assistance, we'll help you keep your records up to date and accurate, giving you peace of mind and more time to focus on growing your business.

Contact us now to get started!

Are there moments you find yourself asking, “How often should you reconcile your bank account?”

Bank account reconciliation is an essential practice for maintaining financial accuracy and ensuring timely reporting. The task involves comparing your business's accounting records to your bank statement, identifying any discrepancies, and making necessary adjustments.

Through bank account reconciliation, you are sure that your financial records are accurate. Regularly reconciling your bank account not only helps to identify potential errors or fraudulent activity but also provides insight into your company's cash flow. By staying on top of these reconciliations, you can confidently make informed decisions.

With these, let us know the appropriate frequency for reconciling your bank account to achieve your goals and the benefits that come with it.

Bank reconciliation should be done on a regular basis, preferably monthly or quarterly, to ensure accuracy between bank statements and accounting records and to detect any discrepancies or errors.

To help you decide better on how often you should do your business bank reconciliation, let us go through the benefits of the different schedules and the process in doing them.

Performing weekly bank reconciliations can help you maintain up-to-date financial records and monitor your cash flow effectively. By reconciling your bank account and books weekly, you can spot any discrepancies or potential fraud early on, allowing for swift resolution.

Weekly reconciliation assists you in managing your cash account and accounts receivable more effectively, avoiding overdraft fees, and ensuring sufficient funds for accounts payable.

To perform a weekly reconciliation, have a daily balance sheet and bank statement comparison. Identify and resolve any discrepancies, such as bank errors, adjusting journal entries, or unusual transactions. Reconcile each transaction individually to ensure accuracy.

Monthly reconciliation is crucial for tracking and controlling your business's cash flow and financial health. Banks typically send monthly statements for the previous month, making it essential to reconcile your books and bank balance regularly. By performing a monthly reconciliation, you can catch any missed payments, double payments, or accounting errors.

Focus on your daily and weekly cash account balance, and compare it with the bank statement balance. Make sure that outstanding checks, deposits in transit, bank charges, and interest income are all included in the details. If you find any discrepancies, make any necessary adjustments to journal entries or correct calculation errors for accuracy.

Conducting quarterly or annual reconciliations provides an opportunity to review your financial records comprehensively, identifying any possible fraud or accounting errors that may have gone unnoticed during the weekly and monthly processes.

A more in-depth review of your financial records at the end of a quarter or fiscal year allows for a thorough analysis of your cash accounts, accounts payable, and accounts receivable.

Compile the bank statements for the entire quarter or year and compare them with your cash account and general ledger. Review the bank accounts for any unexplained transactions or discrepancies not identified during the weekly or monthly reconciliations. Make any necessary adjusting journal entries to correct discrepancies.

When considering how often to reconcile your bank account, consider the factors below too. These details can influence the best frequency for timely and accurate financial reporting.

Larger businesses with more complex operations may need to reconcile their bank accounts more frequently, as they are likely to have more transactions and a higher risk of fraud or accounting errors. Smaller businesses with fewer transactions, on the other hand, may be able to perform bank reconciliations less frequently, such as on a monthly basis, without sacrificing the accuracy of their financial reporting.

A higher volume of transactions can lead to more potential discrepancies between your cash account and your bank statement. Therefore, if your business has a high volume of transactions, it may be more efficient and accurate to reconcile your bank account more frequently, such as weekly or even daily. Conversely, businesses with lower transaction volumes might find it sufficient to reconcile their accounts on a monthly basis.

The frequency at which your bank provides statements will also influence reconciliation prevalence. Typically, banks send monthly statements, which aligns well with a monthly reconciliation schedule. However, with online banking and access to daily transaction updates, you may choose to reconcile your account more frequently to stay on top of your financial records.

The strength of your internal control processes will play a role in bank reconciliation frequency. Segregation of duties and a thorough review process will allow for timely identification and resolution of discrepancies. You can minimize the risk of fraud and accounting errors whether you choose to reconcile your bank account daily, weekly, or monthly.

Reconciling your bank account regularly for timely and accurate financial reporting will be easier with the various software available. The tools below can help streamline your bank reconciliation process to improve efficiency and reduce errors.

You cannot miss QuickBooks in accounting. This tool offers features for reconciling bank accounts and credit card transactions, making it easier for you to identify discrepancies in your financial records and keeping financial data correct and updated.

Another accounting software that can assist in your reconciliation process is Xero. Xero provides tools for bank reconciliation, allowing you to efficiently track and match transactions. Its bank feed feature also reduces manual effort and increases accuracy.

Sage Intacct offers automated bank reconciliation capabilities. This cloud-based accounting tool helps you streamline the process and identify bank errors or discrepancies in your financial records quickly and efficiently.

BlackLine Account Reconciliation is an enterprise-grade solution that enables users to streamline the reconciliation process, improve productivity, and ensure accuracy.

ReconArt is a comprehensive reconciliation software that provides a unified platform for performing reconciliations across various accounts and sources.

FloQast is an accounting workflow automation platform that includes reconciliation capabilities, facilitating collaboration and ensuring accuracy during the process.

SAP S/4HANA is an integrated enterprise resource planning (ERP) system that includes built-in reconciliation functionality, minimizing manual effort and maximizing efficiency.

By now, you already have an idea on how often you should do your bank reconciliation for your business. But before you get going check out these mistakes and challenges first. By being aware of these common mistakes and challenges, you can ensure a more timely and accurate bank reconciliation process.

Bank account reconciliation is essential for maintaining accurate financial records and identifying discrepancies before they escalate. By reconciling your accounts on a regular basis, you can ensure the integrity of your cash flow and make informed financial decisions.

For seamless bookkeeping and expert assistance with bank reconciliations, consider partnering with us here Unloop. With our range of financial services, from accounts payable, payroll, and tax assistance, we'll help you keep your records up to date and accurate, giving you peace of mind and more time to focus on growing your business.

Contact us now to get started!

Tax collection and calculation can be a complex and overwhelming process for Amazon sellers like you. It’s especially challenging if you are operating across international borders, between the US and Canada. You surely have wondered, "How is tax calculated on Amazon?"

Let us answer that question and provide you with a comprehensive overview of how taxes are calculated on Amazon for transacting between the US and Canada. From explaining the different types of taxes imposed by both countries to outlining the necessary steps for tax collection, this guide will equip you with the knowledge and tools to navigate the tax landscape on Amazon effortlessly and efficiently.

Amazon calculates its tax based on the applicable tax laws and regulations of the jurisdictions where it operates, taking into account factors such as sales, income, and other taxable criteria.

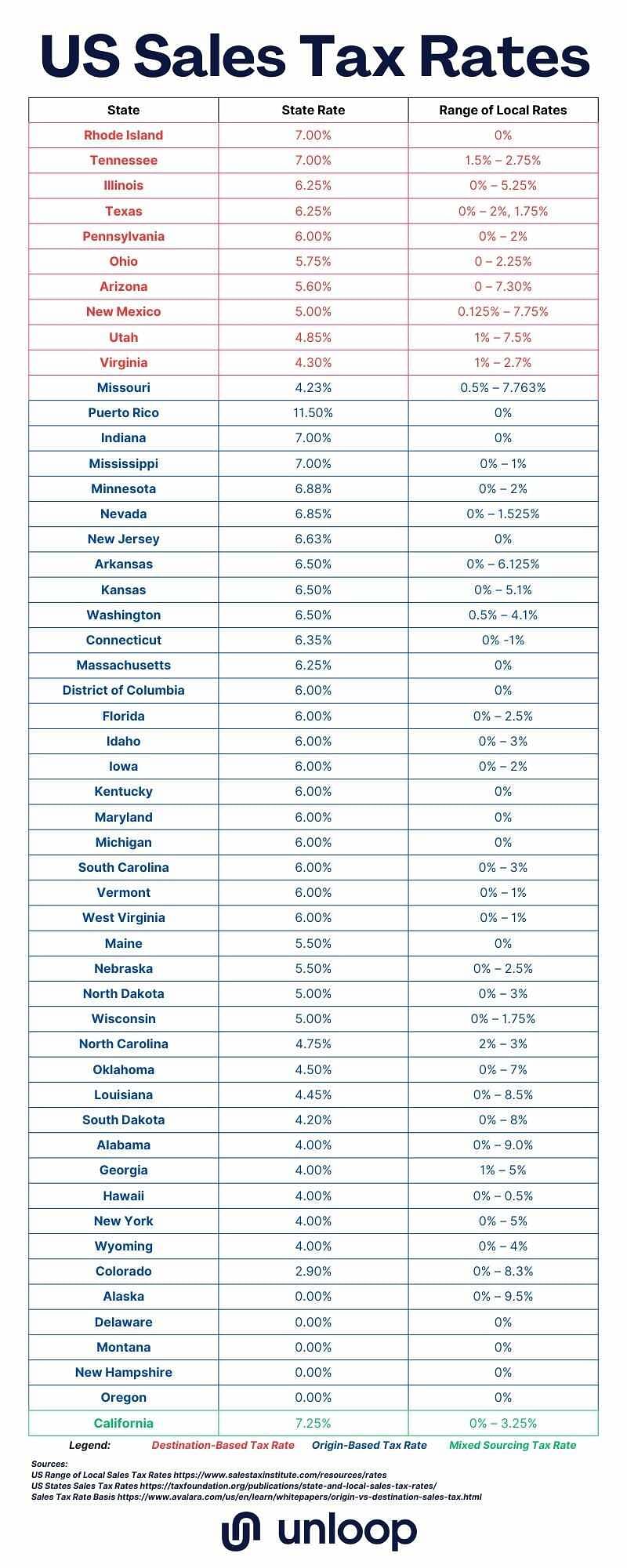

In the United States, tax charges on Amazon orders depend on various factors, such as the type of item or service sold and the shipping destination or origin. Each state has its own set of sales and use tax rates that need to be considered when calculating taxes on transactions.

There are two main factors affecting sales taxes in the US: tax nexus and the Marketplace Facilitator Laws (MPF). Let us know what these two mean for your business.

A nexus is a legal term used to describe a significant presence in a state. It can be based on several factors, such as the location of your offices, employees, warehouses, or fulfillment centers. If your business has a nexus in a state where it sells products, you must collect and remit sales taxes for that state.

You can skip the hassle of collecting and remitting sales taxes on Amazon as the MPF mandates the e-commerce giant do this. Nevertheless, Amazon does not cover local sales taxes not listed on the MPF. In these cases, you have to collect and remit them yourself.

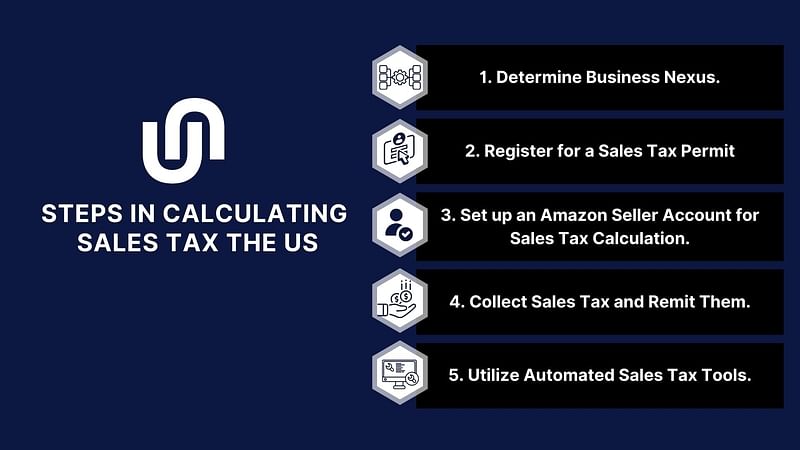

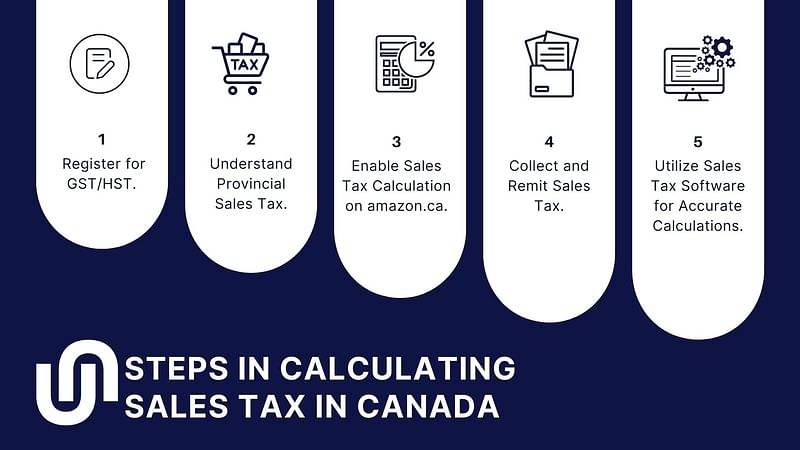

To make your US sales tax calculation and compliance on the platform easier, here are some steps you can follow.

Identify if you have a sales tax nexus in the states where you sell your products. This includes evaluating if you have a physical presence or economic nexus.

Remember that it's illegal to collect Amazon sales tax without a permit, so make sure to register at the state's revenue department.

In your Amazon Seller Central account, set up your sales tax settings. Input the states where you need to collect sales tax, and assign product tax codes to your items to ensure the correct tax rates are applied.

Once your tax settings are configured, Amazon will automatically collect the appropriate sales tax based on the applicable tax rates for each state. Amazon will be responsible for remitting collected sales tax to the relevant tax authorities.

Consider using automated sales tax tools to help you in tracking, sales tax reporting, and filing your sales tax return. These tools can minimize human errors, save time, and help you comply with ever-changing sales tax laws.

Sales tax in Canada includes the different provincial taxes. With different rates applied to individual provinces, you must know the specific tax breakdown. Taxes include the Goods and Services Tax (GST), Provincial Sales Tax (PST), Harmonized Sales Tax (HST), and Quebec Sales Tax (QST). Each of which is determined by the selling price and shipping destination unless stated otherwise.

There are three main types of sales taxes in Canada. Each province and territory has its own PST rate and rules. Some locations have combined GST and PST into an HST.

The GST rate is 5%, and it is applied to most goods and services sold in the country. The collected taxes are used to fund public services and programs.

PST is a sales tax levied by individual provinces in Canada on the retail sale or lease of most goods and some services.

HST, on the other hand, is a combined federal and provincial sales tax that applies in provinces that have chosen to harmonize their sales tax with the federal GST. HST rates can be up to 15%.

To ensure compliance with Canadian tax laws, follow these steps:

To collect and remit sales taxes, register to the Canada Revenue Agency (CRA), especially if your annual sales meet or exceed CAD 30,000.

Research the tax rates and rules for each location where you have a nexus to understand the specific PST or HST rates for each province or territory where you have a tax nexus.

Customize your tax settings in your Amazon Seller Central account to reflect the tax rates and rules of the provinces or territories where you have a nexus.

For tax-liable transactions on Amazon, the platform will automatically collect sales tax from customers at the specified rates in your tax settings. Amazon, through the MPF, files sales tax reports, and remits collected taxes to the CRA accordingly.

To make the sales tax calculation process easier and maintain accuracy, consider using sales tax software. These tools can automatically track tax rates, generate reports, and assist with the filing process if you integrate them into your Amazon Seller Central account.

You are well on your way now that you know how sales taxes work in the US and Canada. To ensure you'll do the tax calculation, collection, and remittance properly, here are some of the best practices you can follow.

To successfully navigate the US and Canadian sales tax on Amazon, stay updated with the latest tax laws and regulations in both countries. US sales tax is based on the combined state and local rates where your order is delivered to or from, while in Canada, businesses are obligated to register and collect GST, PST, or HST.

Using tax automation software can help simplify the tax calculation process on Amazon. These tools integrate with your Amazon Seller Central account and help to ensure accurate sales tax collection, management, and reporting. Through automation, you can minimize errors and allot saved time to essential business tasks.

Some tax software worth trying are the following:

Before selecting a tax software, consider your specific tax needs and consult with a tax professional or advisor to determine which software is best suited for your business.

Proper record-keeping is essential for tax compliance and accurate financial reporting. Maintain detailed records of your sales data, tax rates, and collected taxes. This practice will prove useful when filing sales tax returns, generating tax reports, and ensuring you remit the correct sales tax amount to the relevant tax authorities.

If you're unsure about tax laws or have complex tax situations, don't hesitate to seek professional assistance. Tax experts can help you navigate the intricacies of US and Canadian sales tax regulations, maintain compliance with tax requirements, and guide you in making informed decisions.

Calculating tax accurately on your Amazon sales is crucial to maintaining compliance with tax laws in the US and Canada. With proper tax calculation, you can avoid overcharging or undercharging sales tax on your transactions, ensuring smooth business operations and keeping customers satisfied and loyal.

To implement best practices for effective sales tax calculation, you can get valuable assistance from us here at Unloop. We offer comprehensive guidance on navigating taxes, helping you avoid common pitfalls and maintain compliance with tax authorities.

Take the first step in managing your sales tax obligations effectively by partnering with us. Let our expertise guide you through the complexities of tax calculation and compliance on Amazon, allowing you to focus on growing your business.

Book a call now!

Tax collection and calculation can be a complex and overwhelming process for Amazon sellers like you. It’s especially challenging if you are operating across international borders, between the US and Canada. You surely have wondered, "How is tax calculated on Amazon?"

Let us answer that question and provide you with a comprehensive overview of how taxes are calculated on Amazon for transacting between the US and Canada. From explaining the different types of taxes imposed by both countries to outlining the necessary steps for tax collection, this guide will equip you with the knowledge and tools to navigate the tax landscape on Amazon effortlessly and efficiently.

Amazon calculates its tax based on the applicable tax laws and regulations of the jurisdictions where it operates, taking into account factors such as sales, income, and other taxable criteria.

In the United States, tax charges on Amazon orders depend on various factors, such as the type of item or service sold and the shipping destination or origin. Each state has its own set of sales and use tax rates that need to be considered when calculating taxes on transactions.

There are two main factors affecting sales taxes in the US: tax nexus and the Marketplace Facilitator Laws (MPF). Let us know what these two mean for your business.

A nexus is a legal term used to describe a significant presence in a state. It can be based on several factors, such as the location of your offices, employees, warehouses, or fulfillment centers. If your business has a nexus in a state where it sells products, you must collect and remit sales taxes for that state.

You can skip the hassle of collecting and remitting sales taxes on Amazon as the MPF mandates the e-commerce giant do this. Nevertheless, Amazon does not cover local sales taxes not listed on the MPF. In these cases, you have to collect and remit them yourself.

To make your US sales tax calculation and compliance on the platform easier, here are some steps you can follow.

Identify if you have a sales tax nexus in the states where you sell your products. This includes evaluating if you have a physical presence or economic nexus.

Remember that it's illegal to collect Amazon sales tax without a permit, so make sure to register at the state's revenue department.

In your Amazon Seller Central account, set up your sales tax settings. Input the states where you need to collect sales tax, and assign product tax codes to your items to ensure the correct tax rates are applied.

Once your tax settings are configured, Amazon will automatically collect the appropriate sales tax based on the applicable tax rates for each state. Amazon will be responsible for remitting collected sales tax to the relevant tax authorities.

Consider using automated sales tax tools to help you in tracking, sales tax reporting, and filing your sales tax return. These tools can minimize human errors, save time, and help you comply with ever-changing sales tax laws.

Sales tax in Canada includes the different provincial taxes. With different rates applied to individual provinces, you must know the specific tax breakdown. Taxes include the Goods and Services Tax (GST), Provincial Sales Tax (PST), Harmonized Sales Tax (HST), and Quebec Sales Tax (QST). Each of which is determined by the selling price and shipping destination unless stated otherwise.

There are three main types of sales taxes in Canada. Each province and territory has its own PST rate and rules. Some locations have combined GST and PST into an HST.

The GST rate is 5%, and it is applied to most goods and services sold in the country. The collected taxes are used to fund public services and programs.

PST is a sales tax levied by individual provinces in Canada on the retail sale or lease of most goods and some services.

HST, on the other hand, is a combined federal and provincial sales tax that applies in provinces that have chosen to harmonize their sales tax with the federal GST. HST rates can be up to 15%.

To ensure compliance with Canadian tax laws, follow these steps:

To collect and remit sales taxes, register to the Canada Revenue Agency (CRA), especially if your annual sales meet or exceed CAD 30,000.

Research the tax rates and rules for each location where you have a nexus to understand the specific PST or HST rates for each province or territory where you have a tax nexus.

Customize your tax settings in your Amazon Seller Central account to reflect the tax rates and rules of the provinces or territories where you have a nexus.

For tax-liable transactions on Amazon, the platform will automatically collect sales tax from customers at the specified rates in your tax settings. Amazon, through the MPF, files sales tax reports, and remits collected taxes to the CRA accordingly.

To make the sales tax calculation process easier and maintain accuracy, consider using sales tax software. These tools can automatically track tax rates, generate reports, and assist with the filing process if you integrate them into your Amazon Seller Central account.

You are well on your way now that you know how sales taxes work in the US and Canada. To ensure you'll do the tax calculation, collection, and remittance properly, here are some of the best practices you can follow.

To successfully navigate the US and Canadian sales tax on Amazon, stay updated with the latest tax laws and regulations in both countries. US sales tax is based on the combined state and local rates where your order is delivered to or from, while in Canada, businesses are obligated to register and collect GST, PST, or HST.

Using tax automation software can help simplify the tax calculation process on Amazon. These tools integrate with your Amazon Seller Central account and help to ensure accurate sales tax collection, management, and reporting. Through automation, you can minimize errors and allot saved time to essential business tasks.

Some tax software worth trying are the following:

Before selecting a tax software, consider your specific tax needs and consult with a tax professional or advisor to determine which software is best suited for your business.

Proper record-keeping is essential for tax compliance and accurate financial reporting. Maintain detailed records of your sales data, tax rates, and collected taxes. This practice will prove useful when filing sales tax returns, generating tax reports, and ensuring you remit the correct sales tax amount to the relevant tax authorities.

If you're unsure about tax laws or have complex tax situations, don't hesitate to seek professional assistance. Tax experts can help you navigate the intricacies of US and Canadian sales tax regulations, maintain compliance with tax requirements, and guide you in making informed decisions.

Calculating tax accurately on your Amazon sales is crucial to maintaining compliance with tax laws in the US and Canada. With proper tax calculation, you can avoid overcharging or undercharging sales tax on your transactions, ensuring smooth business operations and keeping customers satisfied and loyal.

To implement best practices for effective sales tax calculation, you can get valuable assistance from us here at Unloop. We offer comprehensive guidance on navigating taxes, helping you avoid common pitfalls and maintain compliance with tax authorities.

Take the first step in managing your sales tax obligations effectively by partnering with us. Let our expertise guide you through the complexities of tax calculation and compliance on Amazon, allowing you to focus on growing your business.

Book a call now!

Taxes can be very challenging because they're very complicated and daunting. It can feel like you pay too much attention to too many things—all at once. Fortunately, the standard deduction is there to simplify things and lessen one's taxable income.

In this article, we will dive into what the standard deduction is, who is eligible for it, and how much it's worth in the federal income tax system this 2023.

The standard deduction is the government's way of conveniently lessening people's taxes. It works by providing a set deductible income per annual accounting period to decrease a payer's taxable income. Standard deduction eliminates the hassle of itemizing deductions annually and gives the lower class more breathing room for taxes.

Age, filing status, and income are the three critical characteristics from your taxpayer's profile that ensure standard deductions are levied fairly by the government. Let’s discuss them one by one.

Age, while not a requirement by the IRS or any related government agencies for tax return filing, can play a role in your standard deductions. For example, being over sixty-five lets taxpayers claim the standard deduction with an additional deduction amount. The same applies to taxpayers who are married and filing jointly, with at least one of them being above sixty-five years old.

Your filing status also affects the standard deduction and whether or not you can use it instead of itemizing deductions. For example, single filers have different standard deductions from married filers, and usually, married filers are given a bigger standard deduction.

Those married filing jointly must decide whether or not to use the standard deduction or lessen their taxable income using itemized deductions instead. For example, if a spouse itemizes deductions, their partner must follow suit. The same goes for the standard deduction.

But this does not mean all married taxpayers are required to file together; taxpayers married filing separately can still file their taxes without following their spouse's preference.

Since the standard deduction decreases your overall taxable income, your earnings play a huge role in determining it. This can be done by subtracting the year's rate of the standard deduction from your income, creating tax exemption, and lowering your overall r income tax.

Using your income also makes using the standard deduction advantageous compared to itemized deductions since the standard deduction is easier. Using your income provides you with a much larger deduction amount than itemizing each qualifying expense.

While age, filing status, and income significantly impact your standard deduction, the rate can still change due to other factors. Here are some characteristics that warrant an increase in standard deduction:

On the other hand, being declared dependent on someone else's federal income tax return reduces one's standard deduction instead of increasing it.

As mentioned in the section about spouses, taxpayers must only use one of the two forms of tax deductions used in a federal tax return for an accounting period: the standard deduction or itemized deductions. But what exactly is the main difference between the two?

| Standard Deduction | Itemized Deduction |

If you choose instead to itemize deductions instead of using the standard deduction, here are some expenses that qualify for tax cuts.

The standard deduction and itemized deductions are essentially the same—they both give people tax cuts and provide them with a fair way of deducting taxes. However, most people tend to gravitate towards using the standard deduction since it usually grants a larger amount, especially after the 2017 Tax Cuts and Job Acts, which inflated the standard deduction and lessened incentives for itemized deductions.

So, in a way, there is no better method of lessening your tax bill. What you can do is calculate your tax bill using both methods and choose the larger amount to ensure you maximize your right to minimize your taxes.

No, the standard deduction rate is not fixed; it changes yearly, as mandated, based on the annual accounting period. What remains the same annually are the qualifications for extra tax deductions, such as differences in filing status and other factors. However, these can change, too, depending again on the tax year.

| Standard Deduction: 2023 Rates |

Taxes, while each citizen's legal responsibility, can be such a hassle. Even with certain deductions in place, it can still be a headache trying to account for them. Fortunately, certain services in the market don't shy away from the numbers.

Unloop is one of the premier accounting services in the market. If you're having trouble with your taxes, try calling us at Unloop—we do taxes, too. Book a call with us here to know more of our services.

Taxes can be very challenging because they're very complicated and daunting. It can feel like you pay too much attention to too many things—all at once. Fortunately, the standard deduction is there to simplify things and lessen one's taxable income.

In this article, we will dive into what the standard deduction is, who is eligible for it, and how much it's worth in the federal income tax system this 2023.

The standard deduction is the government's way of conveniently lessening people's taxes. It works by providing a set deductible income per annual accounting period to decrease a payer's taxable income. Standard deduction eliminates the hassle of itemizing deductions annually and gives the lower class more breathing room for taxes.

Age, filing status, and income are the three critical characteristics from your taxpayer's profile that ensure standard deductions are levied fairly by the government. Let’s discuss them one by one.

Age, while not a requirement by the IRS or any related government agencies for tax return filing, can play a role in your standard deductions. For example, being over sixty-five lets taxpayers claim the standard deduction with an additional deduction amount. The same applies to taxpayers who are married and filing jointly, with at least one of them being above sixty-five years old.

Your filing status also affects the standard deduction and whether or not you can use it instead of itemizing deductions. For example, single filers have different standard deductions from married filers, and usually, married filers are given a bigger standard deduction.

Those married filing jointly must decide whether or not to use the standard deduction or lessen their taxable income using itemized deductions instead. For example, if a spouse itemizes deductions, their partner must follow suit. The same goes for the standard deduction.

But this does not mean all married taxpayers are required to file together; taxpayers married filing separately can still file their taxes without following their spouse's preference.

Since the standard deduction decreases your overall taxable income, your earnings play a huge role in determining it. This can be done by subtracting the year's rate of the standard deduction from your income, creating tax exemption, and lowering your overall r income tax.

Using your income also makes using the standard deduction advantageous compared to itemized deductions since the standard deduction is easier. Using your income provides you with a much larger deduction amount than itemizing each qualifying expense.

While age, filing status, and income significantly impact your standard deduction, the rate can still change due to other factors. Here are some characteristics that warrant an increase in standard deduction:

On the other hand, being declared dependent on someone else's federal income tax return reduces one's standard deduction instead of increasing it.

As mentioned in the section about spouses, taxpayers must only use one of the two forms of tax deductions used in a federal tax return for an accounting period: the standard deduction or itemized deductions. But what exactly is the main difference between the two?

| Standard Deduction | Itemized Deduction |

If you choose instead to itemize deductions instead of using the standard deduction, here are some expenses that qualify for tax cuts.

The standard deduction and itemized deductions are essentially the same—they both give people tax cuts and provide them with a fair way of deducting taxes. However, most people tend to gravitate towards using the standard deduction since it usually grants a larger amount, especially after the 2017 Tax Cuts and Job Acts, which inflated the standard deduction and lessened incentives for itemized deductions.

So, in a way, there is no better method of lessening your tax bill. What you can do is calculate your tax bill using both methods and choose the larger amount to ensure you maximize your right to minimize your taxes.

No, the standard deduction rate is not fixed; it changes yearly, as mandated, based on the annual accounting period. What remains the same annually are the qualifications for extra tax deductions, such as differences in filing status and other factors. However, these can change, too, depending again on the tax year.

| Standard Deduction: 2023 Rates |

Taxes, while each citizen's legal responsibility, can be such a hassle. Even with certain deductions in place, it can still be a headache trying to account for them. Fortunately, certain services in the market don't shy away from the numbers.

Unloop is one of the premier accounting services in the market. If you're having trouble with your taxes, try calling us at Unloop—we do taxes, too. Book a call with us here to know more of our services.

Most capital used in starting a business goes into buying assets for the company. These assets are then used to generate income for the business. However, tangible assets tend to lose value over time and garner a hefty tax bill for a business expense, making it important to learn how to calculate depreciation.

In this article, we'll discuss depreciation, the four ways of calculating it, and the kind of assets you can expect to save money on.

Depreciation is when tangible assets a company invests in loses its value over time due to the typical wear-and-tear of products or equipment. It is an accounting term that determines what an asset is worth. Knowing an item's value is important for businesses to save money from depreciation expenses. It is also essential in monitoring your financial records.

Assets depreciate at different rates. For example, factory equipment may depreciate faster than a company car. There are different ways of calculating depreciation for both. Different factors like asset cost and salvage value come into play to determine the depreciation value of an asset.

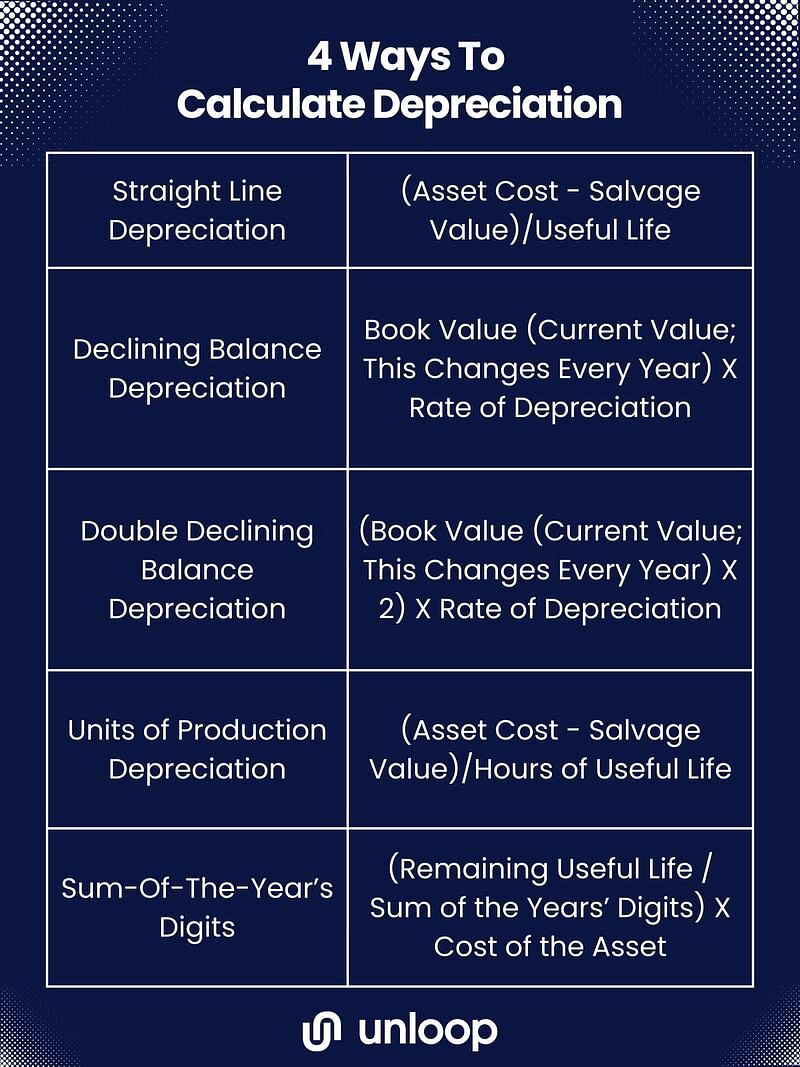

Here are four methods to determine depreciation with their respective formulas.

The straight-line depreciation method is the most common form of calculating depreciation, and it's pretty straightforward. All you have to do is subtract the salvage value from the asset's cost and divide the difference using the asset's useful life in years. The company determines the salvage value, and should be a reasonable amount based on IRS rules.

If a business or organization wants to dispose of assets that lose value quicker, like a company car, the declining balance depreciation method is the best way to go. The declining and double-declining balance methods show assets that depreciate faster, so companies can get more value from depreciation deductions sooner.

To get the depreciation value for a declining balance, you have to multiply the beginning book value of an asset by the rate of depreciation. (To get the depreciation rate, divide 100% by the years of an asset's expected life.)

The same formula applies to the double declining balance method, except you double the amount of the book value. The double declining balance method is typically used to accelerate an asset's depreciation value for taxable income.

Machinery or equipment depreciates at a different rate than other assets because they are used constantly. Their production function defines how much these tools have been used. The method used for depreciating production units is called units of production depreciation.

To get units of production depreciation, follow the straight-line depreciation formula, except use an asset's useful life in hours instead of years.

The sum-of-the-year's digits method, also known as the accelerated depreciation method, is used to depreciate an asset without losing its value, allowing it to retain its value upon disposal. You can get a more even depreciation value over the years using the SYD method.

Getting the depreciation using the SYD method can be complicated. To calculate SYD, divide what's left of an asset's useful life by the sum of years. The SYD is an asset's productive life added together. For example, if an asset is expected to be useful for five years, you can get the SYD by adding 1+2+3+4+5.

Afterward, multiply the asset cost and salvage value. The answer will be your SYD for the first year. Calculating depreciation using the SYD method means having to do it yearly.

In accounting, not all business expenses carrying value are depreciable assets. Here are different kinds of assets in accounting and why or why not they are considered depreciable.

| Tangible Assets | Intangible Assets | Immaterial Assets |

Tangible assets are visible, physical objects and are the only type that can depreciate because they can lose value over time, unlike intangible assets. Some examples of tangible assets are company-owned buildings or houses, vehicles, and equipment.

Intangible assets cannot be seen or touched, like the value of a brand or image and an organization's intellectual property. Intangible assets cannot depreciate and are instead amortized. There are intangible assets that do not depreciate over time. For example, software created by the company will stay valuable since it cannot be destroyed and does not downgrade from use.

Intangible assets are not mentioned in the balance sheet unless they are acquired. For example, if an organization sells its brand image, that will naturally be included in the balance sheet. Certain expenses that contribute to an intangible asset can be credited to the balance sheet and added to an intangible asset's value.

Immaterial assets are tangible or intangible assets acquired for no more than 5% of the purchase price of the said asset. Immaterial assets are bought for a cost too little to be considered significant and can thus be included in miscellaneous or other expenses.

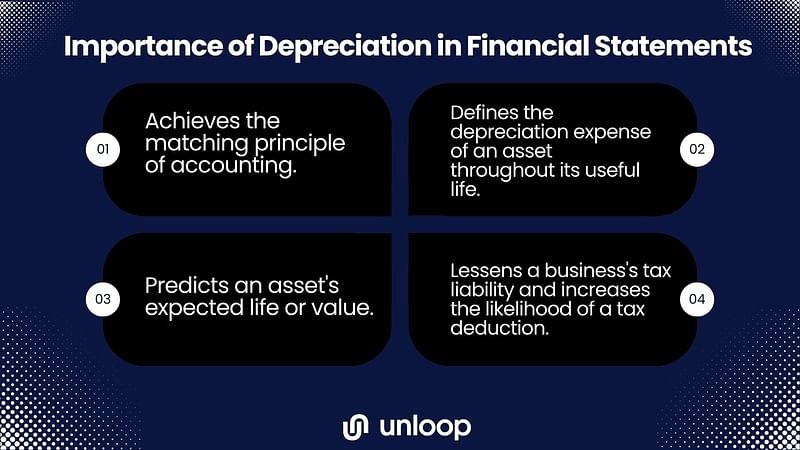

Calculating cumulative depreciation expense is an important task for any business. Depreciation does four things for a business and its financial statements:

Depreciating assets are a valuable accounting detail, especially for tax purposes. If you want to calculate depreciation accurately and make the most out of your company's investments, hire Unloop, one of the prime accounting services in the market.

Let's figure out what your assets’ worth. Book a free discovery call with us here.

Most capital used in starting a business goes into buying assets for the company. These assets are then used to generate income for the business. However, tangible assets tend to lose value over time and garner a hefty tax bill for a business expense, making it important to learn how to calculate depreciation.

In this article, we'll discuss depreciation, the four ways of calculating it, and the kind of assets you can expect to save money on.

Depreciation is when tangible assets a company invests in loses its value over time due to the typical wear-and-tear of products or equipment. It is an accounting term that determines what an asset is worth. Knowing an item's value is important for businesses to save money from depreciation expenses. It is also essential in monitoring your financial records.

Assets depreciate at different rates. For example, factory equipment may depreciate faster than a company car. There are different ways of calculating depreciation for both. Different factors like asset cost and salvage value come into play to determine the depreciation value of an asset.

Here are four methods to determine depreciation with their respective formulas.

The straight-line depreciation method is the most common form of calculating depreciation, and it's pretty straightforward. All you have to do is subtract the salvage value from the asset's cost and divide the difference using the asset's useful life in years. The company determines the salvage value, and should be a reasonable amount based on IRS rules.

If a business or organization wants to dispose of assets that lose value quicker, like a company car, the declining balance depreciation method is the best way to go. The declining and double-declining balance methods show assets that depreciate faster, so companies can get more value from depreciation deductions sooner.

To get the depreciation value for a declining balance, you have to multiply the beginning book value of an asset by the rate of depreciation. (To get the depreciation rate, divide 100% by the years of an asset's expected life.)

The same formula applies to the double declining balance method, except you double the amount of the book value. The double declining balance method is typically used to accelerate an asset's depreciation value for taxable income.

Machinery or equipment depreciates at a different rate than other assets because they are used constantly. Their production function defines how much these tools have been used. The method used for depreciating production units is called units of production depreciation.

To get units of production depreciation, follow the straight-line depreciation formula, except use an asset's useful life in hours instead of years.

The sum-of-the-year's digits method, also known as the accelerated depreciation method, is used to depreciate an asset without losing its value, allowing it to retain its value upon disposal. You can get a more even depreciation value over the years using the SYD method.

Getting the depreciation using the SYD method can be complicated. To calculate SYD, divide what's left of an asset's useful life by the sum of years. The SYD is an asset's productive life added together. For example, if an asset is expected to be useful for five years, you can get the SYD by adding 1+2+3+4+5.

Afterward, multiply the asset cost and salvage value. The answer will be your SYD for the first year. Calculating depreciation using the SYD method means having to do it yearly.

In accounting, not all business expenses carrying value are depreciable assets. Here are different kinds of assets in accounting and why or why not they are considered depreciable.

| Tangible Assets | Intangible Assets | Immaterial Assets |

Tangible assets are visible, physical objects and are the only type that can depreciate because they can lose value over time, unlike intangible assets. Some examples of tangible assets are company-owned buildings or houses, vehicles, and equipment.

Intangible assets cannot be seen or touched, like the value of a brand or image and an organization's intellectual property. Intangible assets cannot depreciate and are instead amortized. There are intangible assets that do not depreciate over time. For example, software created by the company will stay valuable since it cannot be destroyed and does not downgrade from use.

Intangible assets are not mentioned in the balance sheet unless they are acquired. For example, if an organization sells its brand image, that will naturally be included in the balance sheet. Certain expenses that contribute to an intangible asset can be credited to the balance sheet and added to an intangible asset's value.

Immaterial assets are tangible or intangible assets acquired for no more than 5% of the purchase price of the said asset. Immaterial assets are bought for a cost too little to be considered significant and can thus be included in miscellaneous or other expenses.

Calculating cumulative depreciation expense is an important task for any business. Depreciation does four things for a business and its financial statements:

Depreciating assets are a valuable accounting detail, especially for tax purposes. If you want to calculate depreciation accurately and make the most out of your company's investments, hire Unloop, one of the prime accounting services in the market.

Let's figure out what your assets’ worth. Book a free discovery call with us here.

Disclaimer: Please note this article is not financial advice. The purpose of our blog is purely educational, so please consult a professional accountant or financial advisor before making any financial decision.

Many Canadians started online businesses during the lockdown, while some pivoted their traditional brick-and-mortar stores into online ones. Mississauga is no stranger to these businesses. But, these new ecommerce sellers often find it hard to keep track of cash flow, which is why they must hire the best bookkeeping services in Mississauga.

In this blog post, you’ll learn how to choose the right bookkeeping services and the qualities that make an accounting firm the best for your business.

You can choose from plenty of bookkeeping support services in Mississauga. But before committing to one particular service, you have to consider two things.

While there are plenty of bookkeeping providers in Mississauga, some of them may provide certain services only. Before committing to a bookkeeping company, you should assess what specific areas of bookkeeping you need help with.

For example, you may need help managing your financial statements, such as cash flow, accounts payable, and payroll. Those are the easier parts of bookkeeping. But there’s also the rigorous side of it, such as tax planning. The services your business needs will mostly depend on your company’s size.

| <$50,000 monthly revenue | Basic monitoring of cash flow Payroll services |

| >$50,000 monthly revenue | Bookkeeping Tax services |

If your business has less than $50,000 monthly revenue, you’ll most likely just need basic monitoring of cash flow, payroll services, and other areas of financial management. But if you make more than $50,000, you might need to consider bookkeeping and income tax services. This is a good sign because more accounting work means your business has grown more than expected!

Some small business owners opt to do their books on their own. If you’re also thinking of doing that, you need expertise in performing bookkeeping tasks. You should know how to crunch and analyze numbers, and organize and file books. More importantly, you should know the tax requirements in your area.

It sounds like it requires a ton of time and effort, and it does. But as a business owner, you’ll want to focus your energy on operating and growing your business. So, if you need help in managing your books, especially with making a bookkeeping and tax services business plan, it’s a good business move to trust the experts with it.

The two listed above are the questions you should ask yourself before getting bookkeeping and accounting services. After evaluating your business needs, you’re ready to move forward and choose which bookkeeping services you will get. Here are some things to consider during your search.

Canada's high cost of living can be a challenge for many residents, especially business owners. And it’s no secret that accounting and bookkeeping services are costly. After all, this is a fairly technical field, and you’ll want to have professional bookkeepers or a hired professional accountant working on your books to ensure everything is accurate.

Since you’re in the ecommerce industry, it makes sense to work with a company that focuses on providing the best bookkeeping services using the latest accounting software at competitive prices.

Opting for this will lower your bookkeeping costs, eventually giving you more profit.

| 💡A good bookkeeping service should always be available to assist you 24/7. |

If you have any clarifications about the numbers your business is generating, you should be able to ask them and have the answer right away. You won’t get this if you work with traditional bookkeepers and accountants. These people get extremely busy, especially during tax season. You can barely get a hold of them during this time, but it shouldn’t be an excuse to leave you hanging.

The best bookkeeping services can immediately give you clarification when you need it. It gives you peace of mind and understanding about your numbers, leading you to make better business decisions.

Numbers are the backbone of any business. That is why checking and analyzing your financial data monthly is important. Through this, you get a detailed report of how well your business is performing, particularly with your sales and overall expenses. These reports will tell you if your business is still profitable or not.

This is especially important In Mississauga, where businesses are competitive. A good bookkeeping service provider in Mississauga can help you succeed in your online business by providing monthly detailed reports.

Business accounting is a crucial and technical process you should invest in. Understandably, you cannot do it all by yourself. You’ll need the help of a trusted Mississauga bookkeeping service company.

Unloop provides expert accounting, bookkeeping, and even forecasting services targeted toward online businesses in Mississauga. With the help of partner accounting firms and accounting service integrations such as Xero and QuickBooks, we will provide you with the best bookkeeping service in the city.

Ready to focus on growing your business? Book a call with us today, and let us do your books for you!

Disclaimer: Please note this article is not financial advice. The purpose of our blog is purely educational, so please consult a professional accountant or financial advisor before making any financial decision.

Many Canadians started online businesses during the lockdown, while some pivoted their traditional brick-and-mortar stores into online ones. Mississauga is no stranger to these businesses. But, these new ecommerce sellers often find it hard to keep track of cash flow, which is why they must hire the best bookkeeping services in Mississauga.

In this blog post, you’ll learn how to choose the right bookkeeping services and the qualities that make an accounting firm the best for your business.

You can choose from plenty of bookkeeping support services in Mississauga. But before committing to one particular service, you have to consider two things.

While there are plenty of bookkeeping providers in Mississauga, some of them may provide certain services only. Before committing to a bookkeeping company, you should assess what specific areas of bookkeeping you need help with.

For example, you may need help managing your financial statements, such as cash flow, accounts payable, and payroll. Those are the easier parts of bookkeeping. But there’s also the rigorous side of it, such as tax planning. The services your business needs will mostly depend on your company’s size.

| <$50,000 monthly revenue | Basic monitoring of cash flow Payroll services |

| >$50,000 monthly revenue | Bookkeeping Tax services |

If your business has less than $50,000 monthly revenue, you’ll most likely just need basic monitoring of cash flow, payroll services, and other areas of financial management. But if you make more than $50,000, you might need to consider bookkeeping and income tax services. This is a good sign because more accounting work means your business has grown more than expected!

Some small business owners opt to do their books on their own. If you’re also thinking of doing that, you need expertise in performing bookkeeping tasks. You should know how to crunch and analyze numbers, and organize and file books. More importantly, you should know the tax requirements in your area.

It sounds like it requires a ton of time and effort, and it does. But as a business owner, you’ll want to focus your energy on operating and growing your business. So, if you need help in managing your books, especially with making a bookkeeping and tax services business plan, it’s a good business move to trust the experts with it.

The two listed above are the questions you should ask yourself before getting bookkeeping and accounting services. After evaluating your business needs, you’re ready to move forward and choose which bookkeeping services you will get. Here are some things to consider during your search.

Canada's high cost of living can be a challenge for many residents, especially business owners. And it’s no secret that accounting and bookkeeping services are costly. After all, this is a fairly technical field, and you’ll want to have professional bookkeepers or a hired professional accountant working on your books to ensure everything is accurate.

Since you’re in the ecommerce industry, it makes sense to work with a company that focuses on providing the best bookkeeping services using the latest accounting software at competitive prices.

Opting for this will lower your bookkeeping costs, eventually giving you more profit.

| 💡A good bookkeeping service should always be available to assist you 24/7. |

If you have any clarifications about the numbers your business is generating, you should be able to ask them and have the answer right away. You won’t get this if you work with traditional bookkeepers and accountants. These people get extremely busy, especially during tax season. You can barely get a hold of them during this time, but it shouldn’t be an excuse to leave you hanging.

The best bookkeeping services can immediately give you clarification when you need it. It gives you peace of mind and understanding about your numbers, leading you to make better business decisions.

Numbers are the backbone of any business. That is why checking and analyzing your financial data monthly is important. Through this, you get a detailed report of how well your business is performing, particularly with your sales and overall expenses. These reports will tell you if your business is still profitable or not.

This is especially important In Mississauga, where businesses are competitive. A good bookkeeping service provider in Mississauga can help you succeed in your online business by providing monthly detailed reports.

Business accounting is a crucial and technical process you should invest in. Understandably, you cannot do it all by yourself. You’ll need the help of a trusted Mississauga bookkeeping service company.

Unloop provides expert accounting, bookkeeping, and even forecasting services targeted toward online businesses in Mississauga. With the help of partner accounting firms and accounting service integrations such as Xero and QuickBooks, we will provide you with the best bookkeeping service in the city.

Ready to focus on growing your business? Book a call with us today, and let us do your books for you!

Disclaimer: Please note this article is not financial advice. The purpose of our blog is purely educational, so please consult a professional accountant or financial advisor before making any financial decision.

Picture this: You’re an entrepreneur who owns a small business in Toronto. You figure your business will be even better by having a bookkeeper on board. With that in mind, you hop on a computer, open up a search engine, and type “bookkeeping services Toronto”, expecting to find quick and easy bookkeeping solutions.

You check the companies that offer small business bookkeeping in Toronto, and you learn three things:

If you’re reading this, don’t lose hope—this might be the guide you need.

In this blog post, you’ll learn how to find the best accounting and bookkeeping services that will match your business. You’ll also find out how Unloop can help you manage your books without you spending a lot, going through so many steps, and risking your safety.

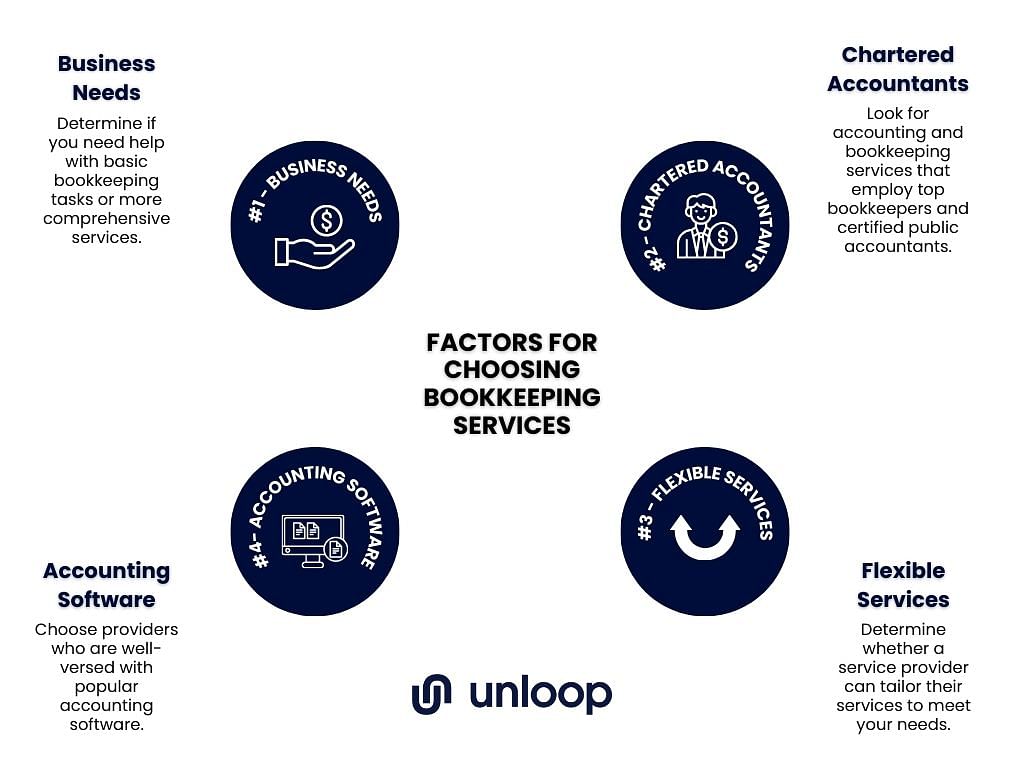

First things first, what are the things you must consider before hiring bookkeeping and accounting services in Toronto? The best bookkeeping service provider for your small business is out there; you just need to evaluate your business needs and size to start.

Here’s a list of factors you should think about:

When choosing small business bookkeeping services, it’s essential to consider your specific needs. Do you operate a brick-and-mortar store or run an online business on Amazon or other e-commerce sites?

| 💡Assess the size and complexity of your business operations and the volume of financial transactions you handle. |

Determine if you need help with basic bookkeeping tasks, such as:

Understanding your business needs will help you find a bookkeeping service in Toronto that aligns with your goals and can provide the necessary support right away.

Another important factor to consider is the expertise and qualifications of the accounting professionals involved. Look for accounting and bookkeeping services that employ top bookkeepers and certified public accountants (CPAs).

According to CPA Ontario, a non-profit organization, they have 99,000 members, including CPAs from Toronto. These experts can provide financial advice, help manage your taxes, and make your accounting and bookkeeping process stress-free.

Consider the tools and accounting software a bookkeeping and accounting service provider uses. Choose providers who are well-versed with popular accounting software such as QuickBooks and Xero.

| 💡Efficient use of accounting software can streamline your financial processes and enhance accuracy in your business’s financial health. |

Every business has unique requirements, and it is essential to choose accounting and bookkeeping services that offer flexibility. Determine whether a service provider can tailor their services to meet your needs.

For instance, small business owners may have seasonal fluctuations, so they may need additional support during peak periods.

They may also look into digitizing their books or adopt cloud-based software—it's important to seek service providers who are well-versed in cloud-based systems such as QuickBooks and Xero.

Now that you know the factors to consider when hiring Toronto bookkeeping services, let’s explore why Unloop could be the best service provider for your business:

For small business owners like you, running a business has to be cost-efficient. You understand that whatever expenses your business has and will have in the future will ultimately affect your bottom line. You want to spend your resources wisely by investing as much in activities that will yield the most revenue possible.

Bookkeeping and accounting, unfortunately, do not come cheap. You know why your small business needs an accountant, but the service’s cost doesn’t justify the investment. You want better pricing—a competitive one. Using technology and resources that allow more competitive pricing, Unloop has an edge above traditional accounting services.

We understand that a small business owner like you knows the value of their time. However, the problem with traditional bookkeeping services is that it takes many back-and-forths before the service can officially start. That’s wasted time that costs not only money but also opportunities.

Traditional accounting firms offering bookkeeping services tend to be bureaucratic. We get it. That’s part of why accounting firms are good at what they do: they follow accounting processes and systems by the book, which can be rigid.

Unloop has identified this inefficiency and adopted a more streamlined process to save a lot of time. Our approach is more agile:

People can do almost anything online. It makes perfect business sense to transfer the cost and burden of bookkeeping to a trustworthy team who can work with you remotely. You get the best pool of talents by outsourcing your bookkeeping to those who can do it well at a cheaper cost from anywhere in the world.

When you outsource your bookkeeping service to a remote team of professionals, there is no need to schedule in-person meetings or travel to a physical location. Remote services allow for scalability, enabling you to pay for the services you need without hiring a dedicated in-house bookkeeper.

This cost-effective approach also benefits small businesses or startups with limited financial resources. These are the things Unloop can do for you. We offer bookkeeping in Toronto, Vaughan, Markham, or anywhere in Canada because we are completely remote.

It’s time for you to take your business in the right direction, wherein you adapt to a world of virtual efficiency. Partner with Unloop and have a global team of talented bookkeepers with much more competitive rates than traditional bookkeeping services and a streamlined, agile bookkeeping process from the get-go.

All the while, you can focus your valuable time on managing your business. Plus, you can ensure that your financial information is in the right hands and up-to-date to help you develop strategic decisions for your business.

Book a call today and let Unloop handle your books accurately, efficiently, and 100% remote!

Disclaimer: Please note this article is not financial advice. The purpose of our blog is purely educational, so please consult a professional accountant or financial advisor before making any financial decision.

Picture this: You’re an entrepreneur who owns a small business in Toronto. You figure your business will be even better by having a bookkeeper on board. With that in mind, you hop on a computer, open up a search engine, and type “bookkeeping services Toronto”, expecting to find quick and easy bookkeeping solutions.

You check the companies that offer small business bookkeeping in Toronto, and you learn three things:

If you’re reading this, don’t lose hope—this might be the guide you need.

In this blog post, you’ll learn how to find the best accounting and bookkeeping services that will match your business. You’ll also find out how Unloop can help you manage your books without you spending a lot, going through so many steps, and risking your safety.

First things first, what are the things you must consider before hiring bookkeeping and accounting services in Toronto? The best bookkeeping service provider for your small business is out there; you just need to evaluate your business needs and size to start.

Here’s a list of factors you should think about:

When choosing small business bookkeeping services, it’s essential to consider your specific needs. Do you operate a brick-and-mortar store or run an online business on Amazon or other e-commerce sites?

| 💡Assess the size and complexity of your business operations and the volume of financial transactions you handle. |

Determine if you need help with basic bookkeeping tasks, such as:

Understanding your business needs will help you find a bookkeeping service in Toronto that aligns with your goals and can provide the necessary support right away.

Another important factor to consider is the expertise and qualifications of the accounting professionals involved. Look for accounting and bookkeeping services that employ top bookkeepers and certified public accountants (CPAs).

According to CPA Ontario, a non-profit organization, they have 99,000 members, including CPAs from Toronto. These experts can provide financial advice, help manage your taxes, and make your accounting and bookkeeping process stress-free.

Consider the tools and accounting software a bookkeeping and accounting service provider uses. Choose providers who are well-versed with popular accounting software such as QuickBooks and Xero.

| 💡Efficient use of accounting software can streamline your financial processes and enhance accuracy in your business’s financial health. |

Every business has unique requirements, and it is essential to choose accounting and bookkeeping services that offer flexibility. Determine whether a service provider can tailor their services to meet your needs.

For instance, small business owners may have seasonal fluctuations, so they may need additional support during peak periods.

They may also look into digitizing their books or adopt cloud-based software—it's important to seek service providers who are well-versed in cloud-based systems such as QuickBooks and Xero.

Now that you know the factors to consider when hiring Toronto bookkeeping services, let’s explore why Unloop could be the best service provider for your business:

For small business owners like you, running a business has to be cost-efficient. You understand that whatever expenses your business has and will have in the future will ultimately affect your bottom line. You want to spend your resources wisely by investing as much in activities that will yield the most revenue possible.

Bookkeeping and accounting, unfortunately, do not come cheap. You know why your small business needs an accountant, but the service’s cost doesn’t justify the investment. You want better pricing—a competitive one. Using technology and resources that allow more competitive pricing, Unloop has an edge above traditional accounting services.

We understand that a small business owner like you knows the value of their time. However, the problem with traditional bookkeeping services is that it takes many back-and-forths before the service can officially start. That’s wasted time that costs not only money but also opportunities.

Traditional accounting firms offering bookkeeping services tend to be bureaucratic. We get it. That’s part of why accounting firms are good at what they do: they follow accounting processes and systems by the book, which can be rigid.

Unloop has identified this inefficiency and adopted a more streamlined process to save a lot of time. Our approach is more agile:

People can do almost anything online. It makes perfect business sense to transfer the cost and burden of bookkeeping to a trustworthy team who can work with you remotely. You get the best pool of talents by outsourcing your bookkeeping to those who can do it well at a cheaper cost from anywhere in the world.

When you outsource your bookkeeping service to a remote team of professionals, there is no need to schedule in-person meetings or travel to a physical location. Remote services allow for scalability, enabling you to pay for the services you need without hiring a dedicated in-house bookkeeper.

This cost-effective approach also benefits small businesses or startups with limited financial resources. These are the things Unloop can do for you. We offer bookkeeping in Toronto, Vaughan, Markham, or anywhere in Canada because we are completely remote.

It’s time for you to take your business in the right direction, wherein you adapt to a world of virtual efficiency. Partner with Unloop and have a global team of talented bookkeepers with much more competitive rates than traditional bookkeeping services and a streamlined, agile bookkeeping process from the get-go.

All the while, you can focus your valuable time on managing your business. Plus, you can ensure that your financial information is in the right hands and up-to-date to help you develop strategic decisions for your business.

Book a call today and let Unloop handle your books accurately, efficiently, and 100% remote!

Distinguished by the North Saskatchewan River, Edmonton is a modern city found in flat prairie scenery. Oil is the prevailing factor in the economy of this beautiful city. Besides that, it also hosts industries related to oil production like engineering and manufacturing. With that said, looking for bookkeeping in Edmonton is not much of a challenge.

Edmonton is the capital city of Alberta. Also known as the Gateway to the North, it is a sparkling city at the heart of the wilderness. It has a popular downtown tourist destination home to world-renowned bakeries, coffee shops, distilleries, and restaurants. Besides that, it has a booming central business district with its high-rise buildings and condominiums.

Home to multitudes of immigrants, making Edmonton a culturally diverse city. With this multi-cultural heritage, the city has many ethnic districts like Chinatown and Little Italy. Downtown Edmonton is also the home of the Avenue of Nations that houses various stores and restaurants of diverse cuisine and cultures.

Suppose you are one of the current entrepreneurs who started a small business in Edmonton; congratulations! After years of back-breaking labor, you finally step out of your comfort zone and go after your passion. Nothing brings you much pleasure in life than following your dream. And you are willing to do everything in your ability to make that vision come to life.

A small business is the extension of its owner’s personality or passion. For example, it is reasonable to assume that a person who loves to bake may open up a bakery someday. Yet, while dreams are enough to motivate you to start a business, it is not enough reason for you to succeed.

It is tough to accept that passion alone is not enough reason for a business to succeed. If you happen to open your business in Edmonton recently, chances are you are doing your own bookkeeping. And if you do, the odds are overwhelming you right now because of all your duties.

Mismanagement is one of the prime culprits why small businesses break down. It is usual for small businesses to have less functional specialists like bookkeepers. If you are a small entrepreneur, you most likely do not make money daily. On top of that, most are not aware of your brand, so make an effort to spread the word. Looking for an Edmonton-based bookkeeping service is probably the least of your worries.

Operating your business is tough enough, to begin with. Then, add in the marketing aspect, and it needs more diligent work. Yet, try to do your bookkeeping, and it becomes unrealistic. There is just no way you can maintain that.

Bookkeeping services are expensive. That is why small entrepreneurs are hesitant to get a bookkeeper. If ever you as a small business owner have the money, you would rather spend it expanding or promoting your business. Bookkeeping in Edmonton usually costs as low as $17 up to $28 an hour.

Virtual bookkeeping services are becoming a more popular alternative to in-person bookkeeping in Edmonton or in any place for that matter. A typical online bookkeeping firm may cost as low as $199 a month, depending on your business needs. It can be daunting a first, but it is a sure-fire way to lower your bookkeeping costs.

Besides that, an online bookkeeping firm can work with you anywhere in the world. So whether you are from Ontario or Vancouver, there is a virtual bookkeeper for your business needs. There are also loads of affordable outsourcing options to choose from.

While you may see bookkeeping as an unnecessary expense, keep in mind that it is an integral part of your success. Not only do bookkeepers manage records, but they also provide you insight to take your business to the next level. Bookkeepers are not an expense. They are an investment.

Edmonton is a city filled with beautiful sights. It is one of Canada’s thriving hotspots for culture, music, and food. It is a fantastic city where dreams are made and eventually come true with the right kind of help.