Question after question and the endless desire to seek the right answers is normal for new Amazon sellers like you. One difficult inquiry you’ll encounter is about taxes, a topic that not everybody is interested in. Still, you need to understand this because it is a huge part of your Amazon store management.

To give you a little background about Amazon taxes, we’ll list five of the most frequently asked questions newbies have. We’ll also include the assistance you can get from an Amazon accounting and bookkeeping agency to know what you can expect. Let’s start!

When talking about Amazon tax, two important things will come up, the Marketplace Tax Collection and the 1099 Amazon tax form. The Marketplace Tax Collection came when the Marketplace Facilitator Law was enacted, which mandates that facilitators like Amazon collect and remit sellers' sales tax.

Meanwhile, Form 1099 is the information submitted by Amazon to the Internal Revenue Service (IRS) every year to report the gross sales income of sellers who are above $20,000 unadjusted Amazon sales income and have more than 200 transactions.

Aside from the Form 1099, here are the other forms on Amazon that are meant for different types of sellers:

You can access Amazon 1099 online through taxcentral.amazon.com by logging into your seller account. The form is readily available beginning January 31 of each year or the day after January 31 if it falls on a holiday.

Amazon also allows the sending of the file via email and even a hard copy through delivery. Just make sure to provide the correct addresses in your tax interview. To avoid missing the hard copy through your mail, always update the address details if there are any changes.

Meanwhile, you can get a preview of the forms W-9, W-8 BEN, W-8BEN-E, and 1042S on the tax interview page.

The Amazon tax interview will involve questions and answers you’ll accomplish on your seller account on Amazon Seller Central.

US sellers need to prepare their business TIN, while non-US sellers must prepare an income tax identification number issued from their country. If you are part of the people and groups who are tax-exempt, you need to prepare your tax-exempt certificate too.

You can use Amazon 1099 for your income tax return. A tax expert can deduct refunds from the unadjusted gross sales for you to pay taxes based on the actual money you’ve earned.

Aside from this, there is plenty of essential data collected by Amazon like sales fulfilled by sellers, sales through Fulfillment by Amazon, shipping payment, gift wrapping payment, and more! When included in the books and reports, these are helpful data that can give you a full view of your business.

It is best to partner with experts if you will use the Amazon 1099 for your income tax return. Bookkeepers and accountants can use the data Amazon gathers to further understand your business finances. In doing so, you can reap these benefits:

Filing income tax returns involves monitoring your income and expenses throughout the tax year, including details from your Amazon 1099. You can skip the worry of paying more than you should because they will deduct the refunds from your gross income jotted on Amazon 1099. Bookkeepers will ensure all details in your books are accurate.

By keeping all your data in a single software, tracking will be easier. A bookkeeping and accounting agency can integrate their software with Amazon to extract data the platform provides, like inventory information, sales, shipping costs, and fulfillment charges.

After all the data is in the books, an Amazon accountant and bookkeeper will work together to create financial reports. Report generation is easier because the agency has reliable bookkeeping and accounting software. As a business just starting out, you should check your store’s financial health as often as possible to enact necessary adjustments or continue best practices.

As an Amazon seller, taxes and obligations will be a part of your life. This includes understanding the different Amazon tax forms, what’s included in them, which one you need, and how to accomplish them.

It is also important for you to know that you can make the most of the financial data you get from Amazon with the help of a bookkeeping and accounting agency. At Unloop, we can help you file your income tax returns, integrate with accounting and bookkeeping software, and make sense of your data through reports. So book a call with us now to learn more about how we can help you manage your Amazon business!

Question after question and the endless desire to seek the right answers is normal for new Amazon sellers like you. One difficult inquiry you’ll encounter is about taxes, a topic that not everybody is interested in. Still, you need to understand this because it is a huge part of your Amazon store management.

To give you a little background about Amazon taxes, we’ll list five of the most frequently asked questions newbies have. We’ll also include the assistance you can get from an Amazon accounting and bookkeeping agency to know what you can expect. Let’s start!

When talking about Amazon tax, two important things will come up, the Marketplace Tax Collection and the 1099 Amazon tax form. The Marketplace Tax Collection came when the Marketplace Facilitator Law was enacted, which mandates that facilitators like Amazon collect and remit sellers' sales tax.

Meanwhile, Form 1099 is the information submitted by Amazon to the Internal Revenue Service (IRS) every year to report the gross sales income of sellers who are above $20,000 unadjusted Amazon sales income and have more than 200 transactions.

Aside from the Form 1099, here are the other forms on Amazon that are meant for different types of sellers:

You can access Amazon 1099 online through taxcentral.amazon.com by logging into your seller account. The form is readily available beginning January 31 of each year or the day after January 31 if it falls on a holiday.

Amazon also allows the sending of the file via email and even a hard copy through delivery. Just make sure to provide the correct addresses in your tax interview. To avoid missing the hard copy through your mail, always update the address details if there are any changes.

Meanwhile, you can get a preview of the forms W-9, W-8 BEN, W-8BEN-E, and 1042S on the tax interview page.

The Amazon tax interview will involve questions and answers you’ll accomplish on your seller account on Amazon Seller Central.

US sellers need to prepare their business TIN, while non-US sellers must prepare an income tax identification number issued from their country. If you are part of the people and groups who are tax-exempt, you need to prepare your tax-exempt certificate too.

You can use Amazon 1099 for your income tax return. A tax expert can deduct refunds from the unadjusted gross sales for you to pay taxes based on the actual money you’ve earned.

Aside from this, there is plenty of essential data collected by Amazon like sales fulfilled by sellers, sales through Fulfillment by Amazon, shipping payment, gift wrapping payment, and more! When included in the books and reports, these are helpful data that can give you a full view of your business.

It is best to partner with experts if you will use the Amazon 1099 for your income tax return. Bookkeepers and accountants can use the data Amazon gathers to further understand your business finances. In doing so, you can reap these benefits:

Filing income tax returns involves monitoring your income and expenses throughout the tax year, including details from your Amazon 1099. You can skip the worry of paying more than you should because they will deduct the refunds from your gross income jotted on Amazon 1099. Bookkeepers will ensure all details in your books are accurate.

By keeping all your data in a single software, tracking will be easier. A bookkeeping and accounting agency can integrate their software with Amazon to extract data the platform provides, like inventory information, sales, shipping costs, and fulfillment charges.

After all the data is in the books, an Amazon accountant and bookkeeper will work together to create financial reports. Report generation is easier because the agency has reliable bookkeeping and accounting software. As a business just starting out, you should check your store’s financial health as often as possible to enact necessary adjustments or continue best practices.

As an Amazon seller, taxes and obligations will be a part of your life. This includes understanding the different Amazon tax forms, what’s included in them, which one you need, and how to accomplish them.

It is also important for you to know that you can make the most of the financial data you get from Amazon with the help of a bookkeeping and accounting agency. At Unloop, we can help you file your income tax returns, integrate with accounting and bookkeeping software, and make sense of your data through reports. So book a call with us now to learn more about how we can help you manage your Amazon business!

Accounting is an essential part of any business. Whether you're an online seller, a small business owner, or the head of a big company, making sense of your business numbers through thorough accounting will show the state of your business's financial health.

However, finances are not many people’s strong suit, and selecting the best expert to assist you is essential. For example, do you need an ecommerce accountant or a CPA? Additionally, are these two professionals even different? This blog post will help you decide who you should hire. We'll differentiate their roles, so you’ll know which professional is suitable for your ecommerce business.

Many people use the term accountant and CPA interchangeably. The confusion is understandable since both jobs involve accounting. But the two roles differ greatly from one another. Although not all accountants are CPAs, all CPAs are accountants.

To help you tell the two apart, consider these significant differences.

Licensure is the primary distinction between an accountant and a CPA. Accountants don't need to take and pass a state-mandated exam to offer their services. However, before becoming a CPA or a certified public accountant, they must first obtain a license.

Furthermore, before CPAs are qualified to take their licensing exam, they should earn a bachelor's degree in financing and accounting. They must also complete rigorous training with specific hours in advanced accounting, auditing, and business courses.

Accountants can have a bachelor's degree in related courses like finance, business management, and accounting. From there, they will gain experience and training from school internships. After getting their diploma, accountants can expand their careers by getting certifications from accredited accounting organizations.

There is no doubt that both professionals can help you with tax planning, returns, and filing. These basic tax services are covered in their training. However, when it comes to taxation laws and codes, a CPA has a more in-depth understanding.

Also, only CPAs can represent a business in front of the IRS. There are times, especially with big companies, when a business gets audited. Only CPAs can answer for your business and sign tax documents when necessary.

A governing body handles certified public accountants. Naturally, organizations have strict regulations and requirements to follow. The American Institute of Certified Public Accountants establish these professional standards, which fall under five broad categories and include:

A key CPA responsibility that accountants cannot do is act as fiduciaries for their clients. This means that an individual or an organization is legally allowed to represent and has authority on behalf of their client's best interest.

If you need representation in front of banks, board members, and government auditors, you should hire a licensed CPA.

Although ecommerce accountants don't have the exact detailed and rigorous training as CPAs, they still have significant roles to play that could benefit ecommerce business owners. Here are some duties they do so you can see if they are suited for your business.

There are many financial statements accountants should handle. There are the balance sheets, profits and loss statements, sales and expense reports, tax return forms, and many more. An accountant should be able to organize financial documents, create copies, and keep them secured and prepared for analysis.

Small business owners can rely on accountants to do accurate financial analysis for their businesses. Since small businesses don't involve many departments, owners can ask for financial advice from their accountants. In addition, ecommerce clients often turn to professionals when it comes to decision-making involving finances, and accountants should be able to help with situations like that.

Financial reporting is essential for an ecommerce company to know the status of its business health. It is an accountant's duty to make these reports in a timely manner. For example, inventory management reports should be done at least once a month to know the exact number of your products.

Reports like these can also determine which products are fast selling and which stay in storage longer. As a result, timely financial data assists businesses in making better corporate decisions. Furthermore, in some situations, these reports are presented to board members, so they should always be prepared beforehand to ensure their accuracy and validity.

You can expect that CPAs can cover the roles and responsibilities of accountants. But with more training, they can offer more services. Let's look at the duties that CPAs can provide for your business.

Accounting services are broad, but a CPA understands and can perform all of the tasks if needed by the business. CPAs are interested in the company's bigger picture and focus their expertise on ensuring that their client's financial and business goals are achieved. Furthermore, CPAs ensure that the money circulates around the business well, so that all business functions are running.

CPAs spend most of their time researching the business and diving into financial data to analyze its performance. Research can identify the strengths of a business and develop them. Furthermore, it can pinpoint weaknesses and potential issues.

You can think of the CPA as the head of all the accountants in one company. Naturally, bigger companies will need a team of accountants to handle their finances. You can think of the CPA as the head of all the accountants in one company. CPAs make sure they delegate responsibilities properly for the accounting system to function.

Furthermore, it's a CPAs duty to talk with the members of the business. They directly report to higher-ups and different business managers, and update and make them understand the business plans moving forward.

Now that you know the difference between CPAs and accountants, you can decide which professional to hire for your business. There is no doubt that both professionals can help with your finances but choosing the right one can affect your business greatly.

If you're a small business owner, you'll need an ecommerce tax accountant more. Sales tax can be a handful for new business owners, but since the number of financial transactions is not significant, accountants can handle accounting for you.

But when your company expands, it will be advantageous to work with a certified public accountant. They can do more, and backed with their accounting expertise, you will be sure that your business finances stays in good hands. However, allocate money in your budget for CPA. Because of their training and expertise, they will cost more than professional accountants.

Hiring a professional is beneficial for every business. It is just a matter of choosing the correct one for your needs. Accountants and CPAs are almost similar in work, but to ensure that your resources are used effectively, be sure to understand what exactly your company needs.

If you're looking for a reliable accounting firm that will handle the needs of your ecommerce business, Unloop is the ecommerce accounting solution for you. We have a team of dedicated professionals that can help you with your business’s finances. Book a call with us today and learn more about our services now.

Accounting is an essential part of any business. Whether you're an online seller, a small business owner, or the head of a big company, making sense of your business numbers through thorough accounting will show the state of your business's financial health.

However, finances are not many people’s strong suit, and selecting the best expert to assist you is essential. For example, do you need an ecommerce accountant or a CPA? Additionally, are these two professionals even different? This blog post will help you decide who you should hire. We'll differentiate their roles, so you’ll know which professional is suitable for your ecommerce business.

Many people use the term accountant and CPA interchangeably. The confusion is understandable since both jobs involve accounting. But the two roles differ greatly from one another. Although not all accountants are CPAs, all CPAs are accountants.

To help you tell the two apart, consider these significant differences.

Licensure is the primary distinction between an accountant and a CPA. Accountants don't need to take and pass a state-mandated exam to offer their services. However, before becoming a CPA or a certified public accountant, they must first obtain a license.

Furthermore, before CPAs are qualified to take their licensing exam, they should earn a bachelor's degree in financing and accounting. They must also complete rigorous training with specific hours in advanced accounting, auditing, and business courses.

Accountants can have a bachelor's degree in related courses like finance, business management, and accounting. From there, they will gain experience and training from school internships. After getting their diploma, accountants can expand their careers by getting certifications from accredited accounting organizations.

There is no doubt that both professionals can help you with tax planning, returns, and filing. These basic tax services are covered in their training. However, when it comes to taxation laws and codes, a CPA has a more in-depth understanding.

Also, only CPAs can represent a business in front of the IRS. There are times, especially with big companies, when a business gets audited. Only CPAs can answer for your business and sign tax documents when necessary.

A governing body handles certified public accountants. Naturally, organizations have strict regulations and requirements to follow. The American Institute of Certified Public Accountants establish these professional standards, which fall under five broad categories and include:

A key CPA responsibility that accountants cannot do is act as fiduciaries for their clients. This means that an individual or an organization is legally allowed to represent and has authority on behalf of their client's best interest.

If you need representation in front of banks, board members, and government auditors, you should hire a licensed CPA.

Although ecommerce accountants don't have the exact detailed and rigorous training as CPAs, they still have significant roles to play that could benefit ecommerce business owners. Here are some duties they do so you can see if they are suited for your business.

There are many financial statements accountants should handle. There are the balance sheets, profits and loss statements, sales and expense reports, tax return forms, and many more. An accountant should be able to organize financial documents, create copies, and keep them secured and prepared for analysis.

Small business owners can rely on accountants to do accurate financial analysis for their businesses. Since small businesses don't involve many departments, owners can ask for financial advice from their accountants. In addition, ecommerce clients often turn to professionals when it comes to decision-making involving finances, and accountants should be able to help with situations like that.

Financial reporting is essential for an ecommerce company to know the status of its business health. It is an accountant's duty to make these reports in a timely manner. For example, inventory management reports should be done at least once a month to know the exact number of your products.

Reports like these can also determine which products are fast selling and which stay in storage longer. As a result, timely financial data assists businesses in making better corporate decisions. Furthermore, in some situations, these reports are presented to board members, so they should always be prepared beforehand to ensure their accuracy and validity.

You can expect that CPAs can cover the roles and responsibilities of accountants. But with more training, they can offer more services. Let's look at the duties that CPAs can provide for your business.

Accounting services are broad, but a CPA understands and can perform all of the tasks if needed by the business. CPAs are interested in the company's bigger picture and focus their expertise on ensuring that their client's financial and business goals are achieved. Furthermore, CPAs ensure that the money circulates around the business well, so that all business functions are running.

CPAs spend most of their time researching the business and diving into financial data to analyze its performance. Research can identify the strengths of a business and develop them. Furthermore, it can pinpoint weaknesses and potential issues.

You can think of the CPA as the head of all the accountants in one company. Naturally, bigger companies will need a team of accountants to handle their finances. You can think of the CPA as the head of all the accountants in one company. CPAs make sure they delegate responsibilities properly for the accounting system to function.

Furthermore, it's a CPAs duty to talk with the members of the business. They directly report to higher-ups and different business managers, and update and make them understand the business plans moving forward.

Now that you know the difference between CPAs and accountants, you can decide which professional to hire for your business. There is no doubt that both professionals can help with your finances but choosing the right one can affect your business greatly.

If you're a small business owner, you'll need an ecommerce tax accountant more. Sales tax can be a handful for new business owners, but since the number of financial transactions is not significant, accountants can handle accounting for you.

But when your company expands, it will be advantageous to work with a certified public accountant. They can do more, and backed with their accounting expertise, you will be sure that your business finances stays in good hands. However, allocate money in your budget for CPA. Because of their training and expertise, they will cost more than professional accountants.

Hiring a professional is beneficial for every business. It is just a matter of choosing the correct one for your needs. Accountants and CPAs are almost similar in work, but to ensure that your resources are used effectively, be sure to understand what exactly your company needs.

If you're looking for a reliable accounting firm that will handle the needs of your ecommerce business, Unloop is the ecommerce accounting solution for you. We have a team of dedicated professionals that can help you with your business’s finances. Book a call with us today and learn more about our services now.

Disclaimer: Please note this article is not financial advice. The purpose of our blog is purely educational, so please consult a professional accountant or financial advisor before making any financial decision.

When it comes to selling products on Amazon, it's crucial for Canadian sellers to understand their income tax obligations. With the rise in online businesses and the increasing popularity of Amazon as a selling platform, you need to know the details and pay the right amount each time.

This article aims to provide Canadian Amazon sellers with a general overview of Amazon seller income tax in Canada. We hope to equip eCommerce sellers like you with the necessary knowledge in securing tax obligations and maximizing business profits.

Here are 8 frequently asked questions, answered:

A sales tax is a value-added consumption tax included in the sales price of goods and services. The sales tax is paid at the buyer's expense, which the seller must file to the appropriate tax authorities.

The Canadian government imposes three different taxes for the computation of a sales tax:

The federal goods and services tax, or GST, is a value-added tax imposed by the government on goods and services. The standard rate for the GST is 5%.

Provincial sales tax, or PST, on the other hand, is a different value-added tax levied locally on the same goods and services that business owners have sold. The rate for the PST is 6%-7%.

The Harmonized Sales Tax (HST) is a uniform rate for five of the thirteen provinces and territories of the Canadian government. In provinces following the HST, the GST or the provincial sales tax PST do not apply.

Instead, there is a single rate for all five provinces, which is 15% (except for Ontario, which charges a 13% sales tax). With the harmonized sales tax (HST), you only need to file one (1) tax return for all five provinces, removing the hassle of doing your taxes.

The Quebec Sales Tax is similar to the Canadian provincial sales taxes (PST) in function, with only the rate being different. If the provincial sales tax is at 6%-7%, then the Quebec sales tax is at 9.975%

The sales tax, while consistent among countries as an attachment to purchasing goods and services, comes in different computations depending on a nation's tax policy.

Now, here's where it can get confusing. You can compute Canada's sales tax in three ways:

First, there is the standard federal sales tax plus provincial taxes. In these provinces, you must add the federal goods and services tax to the local taxes. For example, the sales tax in British Columbia and Manitoba is 12%, coming from a federal sales tax of 5% and provincial taxes of 7%.

Next, some provinces do not impose provincial sales taxes and instead collect only the federal sales tax of 5%. Such provinces include:

Finally, there is the HST. Since the federal taxes and local taxes no longer apply, you can mark your sales tax in provinces under the HST at 15% (except Ontario, with an HST rate of 13%).

Check out the different Canadian sales tax rates below for the specifics:

| Provinces Using Harmonized Sales Tax |

| Newfoundland/Labrador (15%)New Brunswick (15%)Nova Scotia (15%)Ontario (13%)Prince Edward Island (15%) |

| Provinces Using Goods and Services Tax + Provincial Sales Tax |

| British Columbia (12%)Quebec (14.975%)Saskatchewan (11%)Manitoba (12%) |

| Provinces Using Goods and Services Tax Only |

| Alberta (5%)Northwest Territories (5%)Nunavut (5%)Yukon (5%) |

Marketplace facilitators (MPF) handle tax work for third-party sellers. MPF legislation defines ab MPF as a marketplace that allows third-party sellers to sell physical and digital property, goods, and services online.

Amazon, being an MPF, is now responsible for calculating, collecting taxes, and remitting Canadian taxes for their third-party Amazon sellers on taxable sales covered by MPF legislation.

Fulfilling your tax obligations as a Canadian seller can be tedious, but it’s a must. Failure to file and remit sales taxes could lead to criminal charges and could foresee the end of your time as a business owner.

Canadian eCommerce sellers or international sellers have to pay GST/HST.

As the business owner of a Canadian company, you're obliged to pay your Canadian taxes. But for your sales to be taxable, you'll have to open a sales tax account with the Canada Revenue Agency, also known as a GST/HST account.

If you're a Canadian seller with worldwide business income less than or equal to $30,000 for a period of 12 months, you're considered a small supplier and are prohibited from filing for and charging sales taxes. You can collect sales tax and remit on the product or service that surpasses $30,000.

Foreign Amazon sellers with a gross income of over $30,000 in Canadian sales are required to open a sales tax account to pay HST/GST.

Sales tax filing deadline in Canada is April 30, with income tax returns collection beginning around February. Nevertheless, payment for Canadian taxes is usually collected monthly or annually. If your business income is less than $1.5 million in sales, then you can pay annually.

In some provinces, however, the cap is lower. For instance, in Saskatchewan, if you collect less than $3,600, you can pay annually. Then if your taxes are paid on time during the first year, you'll be paying the next few years annually. It would be best to check with the province local rules on monthly, quarterly, or annual tax filing to be sure.

You can pay your GST/HST in three ways:

You can pay your Goods and Services Tax/Harmonized Sales Tax using a financial institution's transaction methods or online banking services. The Canadian Revenue Agency (CRA) has a new online payment method called MyPayment. You can try different payment options using MyPayment. Check their website for different payment options for businesses and individuals.

On the other hand, if you want to pay your GST/HST through a financial institution, use Form RC158, Remittance Voucher - Payment on Filing to pay the amount you owe. These tax forms aren't available online since they come in pre-printed format.

The following tax-related forms are also available:

You can also send your payment by mail. However, payment sent by mail should be under $50,000, regardless of currency. Any mail equal to or above $50,000 should be remitted electronically or through a financial institution.

If you're not paying in Canadian dollars, simply pay the equivalent amount in the available currency.

There you go!

We hope we've provided you with valuable information on Canadian sales taxes, including the different rates and how to compute them.

Remember the recent changes in tax policy that allow Amazon to collect and remit taxes for third-party Amazon sellers. And of course, do not forget that failing to pay taxes can have serious consequences, including criminal charges.

If you need assistance from a tax professional for your Harmonized Sales Tax, Provincial Sales Tax, Quebec Sales Tax, and Goods and Services Tax to keep a clear record to the Canada Revenue agency, partner with Unloop!

We can handle your sales taxes or accounting solutions specifically for your Amazon store. Feel free to contact us. We'd love to discuss your services with you.

Disclaimer: Please note this article is not financial advice. The purpose of our blog is purely educational, so please consult a professional accountant or financial advisor before making any financial decision.

When it comes to selling products on Amazon, it's crucial for Canadian sellers to understand their income tax obligations. With the rise in online businesses and the increasing popularity of Amazon as a selling platform, you need to know the details and pay the right amount each time.

This article aims to provide Canadian Amazon sellers with a general overview of Amazon seller income tax in Canada. We hope to equip eCommerce sellers like you with the necessary knowledge in securing tax obligations and maximizing business profits.

Here are 8 frequently asked questions, answered:

A sales tax is a value-added consumption tax included in the sales price of goods and services. The sales tax is paid at the buyer's expense, which the seller must file to the appropriate tax authorities.

The Canadian government imposes three different taxes for the computation of a sales tax:

The federal goods and services tax, or GST, is a value-added tax imposed by the government on goods and services. The standard rate for the GST is 5%.

Provincial sales tax, or PST, on the other hand, is a different value-added tax levied locally on the same goods and services that business owners have sold. The rate for the PST is 6%-7%.

The Harmonized Sales Tax (HST) is a uniform rate for five of the thirteen provinces and territories of the Canadian government. In provinces following the HST, the GST or the provincial sales tax PST do not apply.

Instead, there is a single rate for all five provinces, which is 15% (except for Ontario, which charges a 13% sales tax). With the harmonized sales tax (HST), you only need to file one (1) tax return for all five provinces, removing the hassle of doing your taxes.

The Quebec Sales Tax is similar to the Canadian provincial sales taxes (PST) in function, with only the rate being different. If the provincial sales tax is at 6%-7%, then the Quebec sales tax is at 9.975%

The sales tax, while consistent among countries as an attachment to purchasing goods and services, comes in different computations depending on a nation's tax policy.

Now, here's where it can get confusing. You can compute Canada's sales tax in three ways:

First, there is the standard federal sales tax plus provincial taxes. In these provinces, you must add the federal goods and services tax to the local taxes. For example, the sales tax in British Columbia and Manitoba is 12%, coming from a federal sales tax of 5% and provincial taxes of 7%.

Next, some provinces do not impose provincial sales taxes and instead collect only the federal sales tax of 5%. Such provinces include:

Finally, there is the HST. Since the federal taxes and local taxes no longer apply, you can mark your sales tax in provinces under the HST at 15% (except Ontario, with an HST rate of 13%).

Check out the different Canadian sales tax rates below for the specifics:

| Provinces Using Harmonized Sales Tax |

| Newfoundland/Labrador (15%)New Brunswick (15%)Nova Scotia (15%)Ontario (13%)Prince Edward Island (15%) |

| Provinces Using Goods and Services Tax + Provincial Sales Tax |

| British Columbia (12%)Quebec (14.975%)Saskatchewan (11%)Manitoba (12%) |

| Provinces Using Goods and Services Tax Only |

| Alberta (5%)Northwest Territories (5%)Nunavut (5%)Yukon (5%) |

Marketplace facilitators (MPF) handle tax work for third-party sellers. MPF legislation defines ab MPF as a marketplace that allows third-party sellers to sell physical and digital property, goods, and services online.

Amazon, being an MPF, is now responsible for calculating, collecting taxes, and remitting Canadian taxes for their third-party Amazon sellers on taxable sales covered by MPF legislation.

Fulfilling your tax obligations as a Canadian seller can be tedious, but it’s a must. Failure to file and remit sales taxes could lead to criminal charges and could foresee the end of your time as a business owner.

Canadian eCommerce sellers or international sellers have to pay GST/HST.

As the business owner of a Canadian company, you're obliged to pay your Canadian taxes. But for your sales to be taxable, you'll have to open a sales tax account with the Canada Revenue Agency, also known as a GST/HST account.

If you're a Canadian seller with worldwide business income less than or equal to $30,000 for a period of 12 months, you're considered a small supplier and are prohibited from filing for and charging sales taxes. You can collect sales tax and remit on the product or service that surpasses $30,000.

Foreign Amazon sellers with a gross income of over $30,000 in Canadian sales are required to open a sales tax account to pay HST/GST.

Sales tax filing deadline in Canada is April 30, with income tax returns collection beginning around February. Nevertheless, payment for Canadian taxes is usually collected monthly or annually. If your business income is less than $1.5 million in sales, then you can pay annually.

In some provinces, however, the cap is lower. For instance, in Saskatchewan, if you collect less than $3,600, you can pay annually. Then if your taxes are paid on time during the first year, you'll be paying the next few years annually. It would be best to check with the province local rules on monthly, quarterly, or annual tax filing to be sure.

You can pay your GST/HST in three ways:

You can pay your Goods and Services Tax/Harmonized Sales Tax using a financial institution's transaction methods or online banking services. The Canadian Revenue Agency (CRA) has a new online payment method called MyPayment. You can try different payment options using MyPayment. Check their website for different payment options for businesses and individuals.

On the other hand, if you want to pay your GST/HST through a financial institution, use Form RC158, Remittance Voucher - Payment on Filing to pay the amount you owe. These tax forms aren't available online since they come in pre-printed format.

The following tax-related forms are also available:

You can also send your payment by mail. However, payment sent by mail should be under $50,000, regardless of currency. Any mail equal to or above $50,000 should be remitted electronically or through a financial institution.

If you're not paying in Canadian dollars, simply pay the equivalent amount in the available currency.

There you go!

We hope we've provided you with valuable information on Canadian sales taxes, including the different rates and how to compute them.

Remember the recent changes in tax policy that allow Amazon to collect and remit taxes for third-party Amazon sellers. And of course, do not forget that failing to pay taxes can have serious consequences, including criminal charges.

If you need assistance from a tax professional for your Harmonized Sales Tax, Provincial Sales Tax, Quebec Sales Tax, and Goods and Services Tax to keep a clear record to the Canada Revenue agency, partner with Unloop!

We can handle your sales taxes or accounting solutions specifically for your Amazon store. Feel free to contact us. We'd love to discuss your services with you.

Financial forecasting is the backbone of good financial planning. Many things can affect a financial forecast other than numbers and some formulas. Fortunately for business owners, technology makes forecasting easier through financial forecasting software tools.

Businesses use several budgeting and forecasting software to help predict future performance and plan future budgets. To help you choose which is best for your business, we've listed some of the best forecasting software options.

Financial forecasting directly affects your budget planning, business strategy, and investments. Even a structured business model needs financial forecasting to prepare for the future.

It's a big problem when businesses run out of cash or are unprepared for the surge of expenses to keep their business running and retain their clients. Accurate financial forecasts are valuable to every business, whether big or small.

Most businesses start with an Excel spreadsheet to develop their financial forecasting. However, forecasting in spreadsheets can be complicated and restrictive due to the following reasons:

Forecasting in Excel is doable, but it is time-consuming and may not always be reliable. Developers continually make software solutions for more progressive, innovative, and convenient forecasting.

Here are the top budgeting and forecasting software products you should check out.

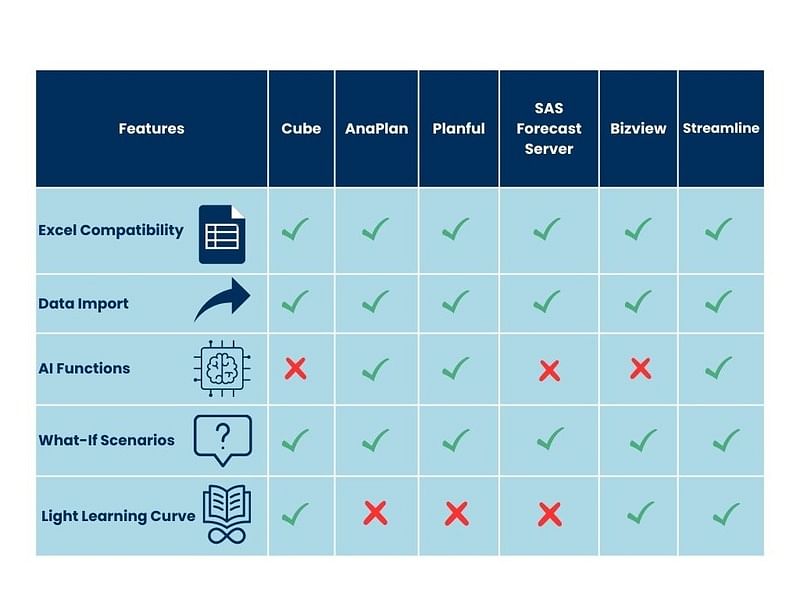

Cube is one of the top-rated forecasting software for businesses. It is the best budgeting and forecasting software for startup businesses that want to quickly transfer their data from manual spreadsheets to forecasting software without studying complicated interfaces. Here is a quick overview of its benefits:

Some of the noteworthy functions of this financial planning software include:

| ✅Automatic data consolidation ✅Bidirectional Microsoft Excel and Google Sheets integrations ✅User-based controls ✅A centralized database for formulas and other data ✅Customizable dashboards and reports |

AnaPlan forecasting software is designed to plan for complex scenarios and do intelligent forecasting for faster and more accurate decision-making. It is ideal for bigger businesses with a dedicated IT team that can handle complex software controls. Here are some key benefits of using AnaPlan:

| ✅It lets you overcome financial and operational planning challenges using user-owned business models. ✅It keeps you updated with the ever-changing marketing conditions using AnaPlan's model engine. ✅Allows you to view business plans on detailed levels to see how they can affect your business in real-time. ✅Increases the accuracy of your decisions and business outcomes by using predictive analysis and what-if analysis. |

Planful is an affordable cloud-based solution for structured and dynamic planning, consolidation, and reporting that suits mid-market companies. Planful offers the following features and benefits:

| ✅ An annual operating plan to help define your company's blueprint for a year. ✅ Workforce planning helps an organization hone employees to work at their best performance. ✅ Scenario analysis to explore every possible option and steer towards it at a moment's notice. ✅ Financial reporting for key financial insights to make better and quicker decisions: This reporting is fully automated and eliminates errors, so you can trust the data you have on hand. |

Planful also has AI-enhanced operations and functions that allow businesses to lessen the number of people they need to hire in the financial department. This reduces expenses in hiring staff.

SAS Forecast Server is one of the popular business forecasting tools because of its ability to generate accurate forecasts quickly. But more than quick forecasts, SAS has many great features to let you be in full control of your business financials:

| The forecasting software has an easy-to-use GUI that can: ✅Generate automatic forecasts in batches or interactively. ✅Build and reconcile forecasts created in varying time intervals. ✅Publish forecasting results via the company's portal, the internet, or hard copy. |

| Its scalability and modeling also offer the following: ✅Freedom to choose the level of automation for the forecasting process ✅Creation of new models by combining two older business models to create more accurate forecasting results ✅Enhanced performance capabilities through the multi-threading of forecasting and diagnostic engines |

The SAS forecasting software has many great and advanced features, which makes this forecasting software good for small businesses and large enterprises. However, it can take some time for business owners to familiarize themselves with the software, but the product has official demo videos to help new users.

Bizview is another cloud-based solution that can streamline your planning, forecasting, and budgeting processes in one software. With a stable internet connection, you can access this software anytime and on any device.

Here are some of the features of Insight Software's Bizview:

| ✅Flexibility, so you can control the software to match your business's needs. ✅It continuously monitors and updates forecasts for the entire year to give your business better insights. ✅It develops accurate financial plans across your entire business, including sales budgets, productions budgets, employee budgets, etc. ✅It allows you to access data from your ERP system and other data sources to create reports without relying on ITs. |

Bizview has an interactive Excel-like interface, so many business owners prefer this software. It is also the most affordable software you can use for small businesses.

Streamline is the leading forecasting software for the first quarter of 2023. Its revenue forecasting processes are realistic, innovative, and quick to ensure that your business is on the right track when planning budgets and making strategic decisions. This budgeting and forecasting software suits big and small businesses.

Here are some of the key features of this forecasting tool:

| ✅The software provides seamless integration of your financial data. You can easily import operational data from your system to Streamline and automatically export financial projections to your ERP system. ✅The software has a scenario planning feature to analyze data and pinpoint potential issues that could happen so you can consider them in your business planning. ✅Financial predictions can involve inventory, cash flow forecasting, and other factors affecting your finances. ✅It has AI-based forecasting capabilities, which ensure 99% accurate budget forecasting at all times. |

There are hundreds of financial budgeting software available for businesses to use. It is just a matter of choosing the right software for your needs. The forecasting tools discussed are some of the best examples you can get for your business. But don't be afraid to explore and find budgeting and forecasting tools to suit your liking and needs.

If you need a budgeting, forecasting, and accounting professional, Unloop can do the job! Our services include revenue forecasting so that we can help small businesses like yours in their growth trajectory.

We use your business's historical data to determine and fix any pain points before they happen. We will also set your business up with an excellent and suitable reporting tool for accurate financial forecasts and continuous planning.

Book a call with our experts today and monitor your financial performance!

Financial forecasting is the backbone of good financial planning. Many things can affect a financial forecast other than numbers and some formulas. Fortunately for business owners, technology makes forecasting easier through financial forecasting software tools.

Businesses use several budgeting and forecasting software to help predict future performance and plan future budgets. To help you choose which is best for your business, we've listed some of the best forecasting software options.

Financial forecasting directly affects your budget planning, business strategy, and investments. Even a structured business model needs financial forecasting to prepare for the future.

It's a big problem when businesses run out of cash or are unprepared for the surge of expenses to keep their business running and retain their clients. Accurate financial forecasts are valuable to every business, whether big or small.

Most businesses start with an Excel spreadsheet to develop their financial forecasting. However, forecasting in spreadsheets can be complicated and restrictive due to the following reasons:

Forecasting in Excel is doable, but it is time-consuming and may not always be reliable. Developers continually make software solutions for more progressive, innovative, and convenient forecasting.

Here are the top budgeting and forecasting software products you should check out.

Cube is one of the top-rated forecasting software for businesses. It is the best budgeting and forecasting software for startup businesses that want to quickly transfer their data from manual spreadsheets to forecasting software without studying complicated interfaces. Here is a quick overview of its benefits:

Some of the noteworthy functions of this financial planning software include:

| ✅Automatic data consolidation ✅Bidirectional Microsoft Excel and Google Sheets integrations ✅User-based controls ✅A centralized database for formulas and other data ✅Customizable dashboards and reports |

AnaPlan forecasting software is designed to plan for complex scenarios and do intelligent forecasting for faster and more accurate decision-making. It is ideal for bigger businesses with a dedicated IT team that can handle complex software controls. Here are some key benefits of using AnaPlan:

| ✅It lets you overcome financial and operational planning challenges using user-owned business models. ✅It keeps you updated with the ever-changing marketing conditions using AnaPlan's model engine. ✅Allows you to view business plans on detailed levels to see how they can affect your business in real-time. ✅Increases the accuracy of your decisions and business outcomes by using predictive analysis and what-if analysis. |

Planful is an affordable cloud-based solution for structured and dynamic planning, consolidation, and reporting that suits mid-market companies. Planful offers the following features and benefits:

| ✅ An annual operating plan to help define your company's blueprint for a year. ✅ Workforce planning helps an organization hone employees to work at their best performance. ✅ Scenario analysis to explore every possible option and steer towards it at a moment's notice. ✅ Financial reporting for key financial insights to make better and quicker decisions: This reporting is fully automated and eliminates errors, so you can trust the data you have on hand. |

Planful also has AI-enhanced operations and functions that allow businesses to lessen the number of people they need to hire in the financial department. This reduces expenses in hiring staff.

SAS Forecast Server is one of the popular business forecasting tools because of its ability to generate accurate forecasts quickly. But more than quick forecasts, SAS has many great features to let you be in full control of your business financials:

| The forecasting software has an easy-to-use GUI that can: ✅Generate automatic forecasts in batches or interactively. ✅Build and reconcile forecasts created in varying time intervals. ✅Publish forecasting results via the company's portal, the internet, or hard copy. |

| Its scalability and modeling also offer the following: ✅Freedom to choose the level of automation for the forecasting process ✅Creation of new models by combining two older business models to create more accurate forecasting results ✅Enhanced performance capabilities through the multi-threading of forecasting and diagnostic engines |

The SAS forecasting software has many great and advanced features, which makes this forecasting software good for small businesses and large enterprises. However, it can take some time for business owners to familiarize themselves with the software, but the product has official demo videos to help new users.

Bizview is another cloud-based solution that can streamline your planning, forecasting, and budgeting processes in one software. With a stable internet connection, you can access this software anytime and on any device.

Here are some of the features of Insight Software's Bizview:

| ✅Flexibility, so you can control the software to match your business's needs. ✅It continuously monitors and updates forecasts for the entire year to give your business better insights. ✅It develops accurate financial plans across your entire business, including sales budgets, productions budgets, employee budgets, etc. ✅It allows you to access data from your ERP system and other data sources to create reports without relying on ITs. |

Bizview has an interactive Excel-like interface, so many business owners prefer this software. It is also the most affordable software you can use for small businesses.

Streamline is the leading forecasting software for the first quarter of 2023. Its revenue forecasting processes are realistic, innovative, and quick to ensure that your business is on the right track when planning budgets and making strategic decisions. This budgeting and forecasting software suits big and small businesses.

Here are some of the key features of this forecasting tool:

| ✅The software provides seamless integration of your financial data. You can easily import operational data from your system to Streamline and automatically export financial projections to your ERP system. ✅The software has a scenario planning feature to analyze data and pinpoint potential issues that could happen so you can consider them in your business planning. ✅Financial predictions can involve inventory, cash flow forecasting, and other factors affecting your finances. ✅It has AI-based forecasting capabilities, which ensure 99% accurate budget forecasting at all times. |

There are hundreds of financial budgeting software available for businesses to use. It is just a matter of choosing the right software for your needs. The forecasting tools discussed are some of the best examples you can get for your business. But don't be afraid to explore and find budgeting and forecasting tools to suit your liking and needs.

If you need a budgeting, forecasting, and accounting professional, Unloop can do the job! Our services include revenue forecasting so that we can help small businesses like yours in their growth trajectory.

We use your business's historical data to determine and fix any pain points before they happen. We will also set your business up with an excellent and suitable reporting tool for accurate financial forecasts and continuous planning.

Book a call with our experts today and monitor your financial performance!

Cash flow forecasting can be tricky—it requires skills, attention to detail, and dedication. But when done right, cash flow forecasting can offer tremendous value and invaluable insight into the future of your startup business or project.

Many organizations face significant challenges while attempting this exercise, but some workarounds can help you achieve success in predicting your financial future with confidence.

In this blog post, we'll explore some common cash flow forecasting challenges and solutions for improving your forecasts' accuracy. With these tips, you'll have valuable information to make better decisions about where to allocate resources and set appropriate expectations for revenue and expenses.

As an owner of a startup business, at the beginning, your cash flow may be slow and manageable using manual bookkeeping and accounting. A common mistake would be sticking to this day-to-day cash flow monitoring system and not forecasting. Seeing only daily cash flow and having no visibility about your company's future income and expenses is like operating a business in the dark.

Understand that cash flow management is essential for all businesses, even startups. Know that with it, you can see how much income and expenses you’ll have daily, weekly, monthly, quarterly, or annually. As a result, you can use the data as the basis of your financial game plans. You can use it to decide the following:

Having limited historical data is common to startups either because owners have failed to store financial data in the past or because the business hasn’t been running for a significant period of time yet. Historical data is the most basic information needed when creating a cash flow forecast, and the absence of these numbers makes the forecast result less reliable.

Despite the absence of historical data, there are still ways to get a reliable cash flow forecast. To begin, whether you lack past numbers because of a personal choice or not, it is time to invest in software and applications to help you track your business finances.

These apps and software can also help you conveniently create simulations, or before and after trials. Use the following data for your forecasts:

The biggest enemy of a cash flow forecast is inaccurate data, which can happen when tracking income and expenses manually. Although Excel sheets are readily available (and free), they may lose your business money in the long run as human errors bring costly damages to your finances.

Inaccurate data leads to making bigger loans, being overconfident in forecasting income, making fewer investments, and saving less—all detrimental to your business growth.

The most efficient workaround to the data inaccuracy problem is bidding goodbye to your company's manual systems. Accept that part of growth is optimizing your bookkeeping and accounting technology so that you can track your finances better.

Accounting software is highly automated, and you can also integrate various apps. As a result, you can minimize or even eradicate manual inputs, which can cause inaccurate data.

If there are a couple of teams in your company, you’ll need input for their income and expenses. This task becomes a roadblock when there is no collaboration between different departments. When different teams do not practise open communication, you might get incomplete or erroneous financial data from them. Another challenge is not having an established system for workflow and data submission processes in the company.

Excellent accountants and bookkeepers need to be well-versed in their tasks or have certifications and training to perform them correctly. On top of that, they should have communication skills and be team players. This is to make sure that they can connect to the various departments in your company to get the needed data. They also need to be forward thinkers to suggest and enact the best systems to make this data acquisition as smooth as possible for everyone.

Expect that a cash flow forecast doesn’t mean you’ll get 100% accuracy, as the following variables are prone to changes:

As a result, the final accounts receivable and payable won’t be exactly as what you forecasted.

The best workaround to ensure that you get the forecast closest to the truth is keeping numbers and data updated. Be in the know with the latest interest and foreign exchange rates. Know if there are changes in sales taxes and other tax dues you need to pay. If there are updates on commodity and raw material prices, they should also be reflected in your forecast. And do not forget about your customers too. Check sales trends to know when your peak sales occur.

Successfully launching a cash flow forecast is not the end of the cash forecasting process, but it becomes a problem if you make it so. As we’ve learned, some variables are subject to change, so if one variable adjusts, the income and expenses will as well. If you keep on using the old data without any adjustments, your business finances will suffer these consequences:

The best way to do a cash flow projection and actual cash flow analysis is through the help of software. An accounting software already has the forecast and the latest data of your business stored. They also have templates to show a comparison of current cash flow and forecast data. With software, generating reports is easier, and you can regularly analyze data to see if you need to optimize your cash flow plans and strategies.

Creating and maintaining a cash flow forecast is a major task for every company. Not having a dedicated team to handle it makes report generation impossible. And if even one is created, there wouldn’t be anyone to update it and let you know the latest data analysis results. Like a snowball, a series of the above mentioned challenges will surely accumulate.

There are plenty of choices a company can go for to hire a bookkeeper and accountant to handle forecasts. An in-house accountant is the traditional choice, but you can also choose to work with remote team members and freelancers. With these choices, building a dedicated team to handle forecasting becomes easier.

Your finance team will ensure your business has a defined forecasting process, an efficient way to acquire and manage data, and the best software to make forecasting cash flow easier and more accurate.

With cash forecasting being so important to any business’s success, startups must understand common challenges and how to avoid them. We hope that these common challenges startups face when forecasting cash flow and some workarounds have helped you. At Unloop, we have seen firsthand how important cash flow forecasts are to businesses. Proper forecasts can help businesses stretch their budgets and stay ahead of payments. With that in mind, take advantage of our forecasting services to experience the power of having a reliable and secure forecasting platform at your fingertips. Call us today!

Cash flow forecasting can be tricky—it requires skills, attention to detail, and dedication. But when done right, cash flow forecasting can offer tremendous value and invaluable insight into the future of your startup business or project.

Many organizations face significant challenges while attempting this exercise, but some workarounds can help you achieve success in predicting your financial future with confidence.

In this blog post, we'll explore some common cash flow forecasting challenges and solutions for improving your forecasts' accuracy. With these tips, you'll have valuable information to make better decisions about where to allocate resources and set appropriate expectations for revenue and expenses.

As an owner of a startup business, at the beginning, your cash flow may be slow and manageable using manual bookkeeping and accounting. A common mistake would be sticking to this day-to-day cash flow monitoring system and not forecasting. Seeing only daily cash flow and having no visibility about your company's future income and expenses is like operating a business in the dark.

Understand that cash flow management is essential for all businesses, even startups. Know that with it, you can see how much income and expenses you’ll have daily, weekly, monthly, quarterly, or annually. As a result, you can use the data as the basis of your financial game plans. You can use it to decide the following:

Having limited historical data is common to startups either because owners have failed to store financial data in the past or because the business hasn’t been running for a significant period of time yet. Historical data is the most basic information needed when creating a cash flow forecast, and the absence of these numbers makes the forecast result less reliable.

Despite the absence of historical data, there are still ways to get a reliable cash flow forecast. To begin, whether you lack past numbers because of a personal choice or not, it is time to invest in software and applications to help you track your business finances.

These apps and software can also help you conveniently create simulations, or before and after trials. Use the following data for your forecasts:

The biggest enemy of a cash flow forecast is inaccurate data, which can happen when tracking income and expenses manually. Although Excel sheets are readily available (and free), they may lose your business money in the long run as human errors bring costly damages to your finances.

Inaccurate data leads to making bigger loans, being overconfident in forecasting income, making fewer investments, and saving less—all detrimental to your business growth.

The most efficient workaround to the data inaccuracy problem is bidding goodbye to your company's manual systems. Accept that part of growth is optimizing your bookkeeping and accounting technology so that you can track your finances better.

Accounting software is highly automated, and you can also integrate various apps. As a result, you can minimize or even eradicate manual inputs, which can cause inaccurate data.

If there are a couple of teams in your company, you’ll need input for their income and expenses. This task becomes a roadblock when there is no collaboration between different departments. When different teams do not practise open communication, you might get incomplete or erroneous financial data from them. Another challenge is not having an established system for workflow and data submission processes in the company.

Excellent accountants and bookkeepers need to be well-versed in their tasks or have certifications and training to perform them correctly. On top of that, they should have communication skills and be team players. This is to make sure that they can connect to the various departments in your company to get the needed data. They also need to be forward thinkers to suggest and enact the best systems to make this data acquisition as smooth as possible for everyone.

Expect that a cash flow forecast doesn’t mean you’ll get 100% accuracy, as the following variables are prone to changes:

As a result, the final accounts receivable and payable won’t be exactly as what you forecasted.

The best workaround to ensure that you get the forecast closest to the truth is keeping numbers and data updated. Be in the know with the latest interest and foreign exchange rates. Know if there are changes in sales taxes and other tax dues you need to pay. If there are updates on commodity and raw material prices, they should also be reflected in your forecast. And do not forget about your customers too. Check sales trends to know when your peak sales occur.

Successfully launching a cash flow forecast is not the end of the cash forecasting process, but it becomes a problem if you make it so. As we’ve learned, some variables are subject to change, so if one variable adjusts, the income and expenses will as well. If you keep on using the old data without any adjustments, your business finances will suffer these consequences:

The best way to do a cash flow projection and actual cash flow analysis is through the help of software. An accounting software already has the forecast and the latest data of your business stored. They also have templates to show a comparison of current cash flow and forecast data. With software, generating reports is easier, and you can regularly analyze data to see if you need to optimize your cash flow plans and strategies.

Creating and maintaining a cash flow forecast is a major task for every company. Not having a dedicated team to handle it makes report generation impossible. And if even one is created, there wouldn’t be anyone to update it and let you know the latest data analysis results. Like a snowball, a series of the above mentioned challenges will surely accumulate.

There are plenty of choices a company can go for to hire a bookkeeper and accountant to handle forecasts. An in-house accountant is the traditional choice, but you can also choose to work with remote team members and freelancers. With these choices, building a dedicated team to handle forecasting becomes easier.

Your finance team will ensure your business has a defined forecasting process, an efficient way to acquire and manage data, and the best software to make forecasting cash flow easier and more accurate.

With cash forecasting being so important to any business’s success, startups must understand common challenges and how to avoid them. We hope that these common challenges startups face when forecasting cash flow and some workarounds have helped you. At Unloop, we have seen firsthand how important cash flow forecasts are to businesses. Proper forecasts can help businesses stretch their budgets and stay ahead of payments. With that in mind, take advantage of our forecasting services to experience the power of having a reliable and secure forecasting platform at your fingertips. Call us today!

Monitoring your business's accounts payable is crucial to determine the state of its financial health. Accurate forecasting allows you to gain control of your cash flow. In addition, knowing when your payments are due builds a good relationship with your suppliers and opens up strategies for money-saving plans for your payables.

Forecasting accounts payable may not be your priority when handling business accounting, but it can benefit your business. In this blog post, we'll talk more about forecasting accounts payable so you know how to do it for your business.

Accounts payable refers to short-term liabilities a business needs to pay off within a year or a shorter time frame. Understanding and seeing your business expenses fully allows you to do the groundwork for building a suitable budget for your business.

Forecasting will help you prepare to meet your payments by considering different scenarios. For example, if the price of raw materials increase or third-party fees change their rates, you can ensure your business can still fulfill its obligations and make wise decisions regarding your business finances.

You can monitor the money going out of your business in several ways. Here are some things you can do to help you build an accurate accounts payable forecast.

The payment patterns for your business are an important piece of information in creating an accurate forecast. Your expenses on payroll and inventory are relatively consistent month to month and easier to track. But always look at past spending data to see accurate patterns.

For example, look at the months you spend more on inventory. Some of your items may be in demand in certain months, so be mindful of that so you can plan your budget accordingly. You can also accumulate your past invoices to have a picture of where your money is going.

Noticing the patterns will also help you see where you can save, which can be good for your cash flow.

Understanding trends in the marketplace, like technological advances and consumer behaviour, will help determine if these changes can affect your business payables. Changes in the industry are quick, and if you're not keen enough to see them, you may fall behind, which can make your forecast less accurate.

You can track some marketing trends by:

Using historical data is advantageous for forecasting because many methods maximize historical data. The most common way of using past data is through extrapolation. However, there's room for error with this method because it doesn't consider the changes that happened in your business.

Statistical modelling is a more accurate method for creating accounts payable forecasts. This method helps business owners identify behavior in ways businesses do their payments and create a forecast based on its current conditions. This forecasting method is the most accurate but requires a huge investment in time and resources.

If you're new to forecasting, it is best to use both methods for the best results. Then, play with the strength of each method to make better business decisions.

You need all the data to create an accurate forecast. That's why it is crucial that you keep track of your invoices and dues. Here are some ways to do it effectively:

Accounting software is a valuable tool for businesses. Think of it as a virtual assistant that handles certain tasks that you can't because your hands are full. For example, you can start with a Microsoft Excel spreadsheet to organize your cash flow in a certain accounting period. Although this may keep things organized, you still have to input data and create financial statements manually when needed.

If you want something more convenient, there are several accounting software you can choose from. These software options can perform basic accounting tasks and even more complex ones. Furthermore, they can produce financial statements like income statements, balance sheets, and other reports in just a few clicks.

Some even have a feature to create financial models for your business based on the data you input into the system. The right accounting software will help create your business's accurate accounts payable forecast.

Knowing how much you need to pay at the end of each period will help you plan your budget. Fortunately, there is a simple calculation method that allows you to get an overview of your expected accounts payables.

Here is how to do it:

Once you have this data, you can simply follow the formula:

(Current liabilities)/(Total operating cash/Number of days) = Expected accounts payable

So, for example, if your business has an outstanding liability of $10,000 and your total

operating cost is $25,000, and you have 25 days to complete your payments. You can calculate your expected payables by:

(10,000)/(25,000/25) = $10,000

You can expect your business needs to pay $10,000 by the end of 25 days.

Forecasting is an optional part of accounting, and some business owners find it unnecessary. However, forecasting is a good move for your business if you want a clearer view of your financial ratios. Here are some benefits of doing it.

The results of the accounts payable forecast are valuable for improving your cash flow forecasting. This will help get key insights into how much of your working capital is available for business growth and investment. In addition, a clear picture of your forecast will help you maximize your working capital more confidently and risk-free.

Nothing makes your suppliers happier than you paying them on time. Forecasting accounts payable will help you see your deliverables ahead of time so you won't incur late payments. In addition, timely payments build trust and good relationships with your suppliers.

Moreover, forecasting helps you identify if you will run into problems with your payments. This way, you can give your suppliers a warning if there's no choice but to delay your payments.

Knowing your expected liabilities will help prevent disruptions in your payments. Understanding how much working capital comes in and out of your business in a specific period will help you eliminate risks and other potential disruptions.

Now that you have an overview of how forecasting accounts payable can benefit your business, you should start planning how you can forecast. Forecasting is not an easy task, so it is better to have a professional handle this for you.

Unloop offers AP forecasting for small ecommerce businesses. Our team of experts will ensure:

Unloop can handle all your accounts payable needs and even other accounting needs. Our team is ready to work with you on your bookkeeping, income tax, payroll, financial forecasts, and accounting. Book a call and work with us today!

Monitoring your business's accounts payable is crucial to determine the state of its financial health. Accurate forecasting allows you to gain control of your cash flow. In addition, knowing when your payments are due builds a good relationship with your suppliers and opens up strategies for money-saving plans for your payables.

Forecasting accounts payable may not be your priority when handling business accounting, but it can benefit your business. In this blog post, we'll talk more about forecasting accounts payable so you know how to do it for your business.

Accounts payable refers to short-term liabilities a business needs to pay off within a year or a shorter time frame. Understanding and seeing your business expenses fully allows you to do the groundwork for building a suitable budget for your business.

Forecasting will help you prepare to meet your payments by considering different scenarios. For example, if the price of raw materials increase or third-party fees change their rates, you can ensure your business can still fulfill its obligations and make wise decisions regarding your business finances.

You can monitor the money going out of your business in several ways. Here are some things you can do to help you build an accurate accounts payable forecast.

The payment patterns for your business are an important piece of information in creating an accurate forecast. Your expenses on payroll and inventory are relatively consistent month to month and easier to track. But always look at past spending data to see accurate patterns.

For example, look at the months you spend more on inventory. Some of your items may be in demand in certain months, so be mindful of that so you can plan your budget accordingly. You can also accumulate your past invoices to have a picture of where your money is going.

Noticing the patterns will also help you see where you can save, which can be good for your cash flow.

Understanding trends in the marketplace, like technological advances and consumer behaviour, will help determine if these changes can affect your business payables. Changes in the industry are quick, and if you're not keen enough to see them, you may fall behind, which can make your forecast less accurate.

You can track some marketing trends by:

Using historical data is advantageous for forecasting because many methods maximize historical data. The most common way of using past data is through extrapolation. However, there's room for error with this method because it doesn't consider the changes that happened in your business.

Statistical modelling is a more accurate method for creating accounts payable forecasts. This method helps business owners identify behavior in ways businesses do their payments and create a forecast based on its current conditions. This forecasting method is the most accurate but requires a huge investment in time and resources.

If you're new to forecasting, it is best to use both methods for the best results. Then, play with the strength of each method to make better business decisions.

You need all the data to create an accurate forecast. That's why it is crucial that you keep track of your invoices and dues. Here are some ways to do it effectively:

Accounting software is a valuable tool for businesses. Think of it as a virtual assistant that handles certain tasks that you can't because your hands are full. For example, you can start with a Microsoft Excel spreadsheet to organize your cash flow in a certain accounting period. Although this may keep things organized, you still have to input data and create financial statements manually when needed.

If you want something more convenient, there are several accounting software you can choose from. These software options can perform basic accounting tasks and even more complex ones. Furthermore, they can produce financial statements like income statements, balance sheets, and other reports in just a few clicks.

Some even have a feature to create financial models for your business based on the data you input into the system. The right accounting software will help create your business's accurate accounts payable forecast.

Knowing how much you need to pay at the end of each period will help you plan your budget. Fortunately, there is a simple calculation method that allows you to get an overview of your expected accounts payables.

Here is how to do it:

Once you have this data, you can simply follow the formula: